HORTER INVESTMENT MANAGEMENT, LLC

Weekly Commentary horterinvestment.com November 26, 2018

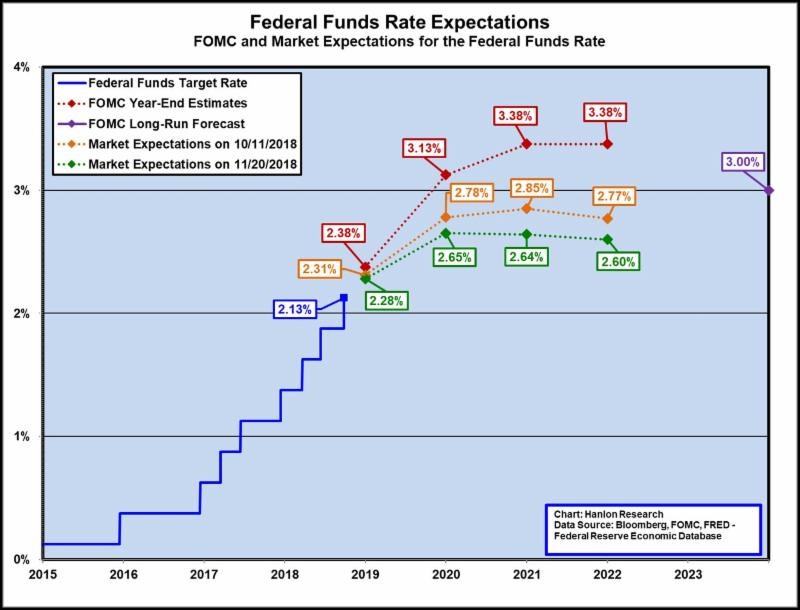

As US recession chances increase, the Fed may deliver fewer rate hikes: Reuters poll

The Federal Reserve is still expected to raise interest rates again next month and three times next year, but a strong majority of economists polled by Reuters over the past week say the risk is it will slow that pace down.

The probability of a U.S. recession in the next two years, while still low, also nudged up to a median 35 percent from 30 percent in the latest monthly Reuters survey of economists taken Nov 13-19. It held at 15 percent for the next 12 months.

While many developed economies are already slowing, growth in the world’s largest economy is still solid, riding the tail-end of a $1.5 trillion tax cut boost, and official unemployment is the lowest in nearly half a century.

But that shine is forecast to start coming off this quarter, with growth slowing more by the end of next year as a trade stand-off with China shows no signs of letting up.

“The economy is facing a growing number of headwinds,

including the lagged effects of previous interest rate rises and dollar strength, the uncertainty of trade protectionism at a time when external demand is slowing, and a sense that the support from the fiscal stimulus will gradually fade,” said James Knightley, chief international economist at ING.

The stock market’s woes could weigh on the holiday shopping season

From turkey to the malls, more than 164 million Americans figured to hit the stores between Thanksgiving and Cyber Monday according to the National Retail Federation. But how will the retailers fare the rest of the holiday season?

“I don’t think the consumer could be healthier,” retail consultant Jan Kniffen told CNBC’s “On the Money” in an interview. “Rising wages, they’re all working, unemployment at a 50-year low, the consumer’s got no problems unless the S&P 500 is a problem.”

In the past two months, stocks have taken a beating with the S&P 500 down around 10 percent. Kniffen said there have been studies done that show “the correlation between retail sales in the holiday season and the S&P 500 are pretty high.” But he’s hoping this year will be different because everything else, including low energy costs and credit scores, is going right.

For the first time ever, the average national FICO score reached 704. Kniffen predicts brick and mortar retailers will see 5.5 percent growth in holiday sales over last year.

The consultant said retailers including Kohl’s, Macy’s, Nordstrom’s and Walmart are putting in place strategies to give consumers what they want, when they want it — such as curbside pickup, returning online orders in stores and buying online with in store pickup.

But all of this costs money.

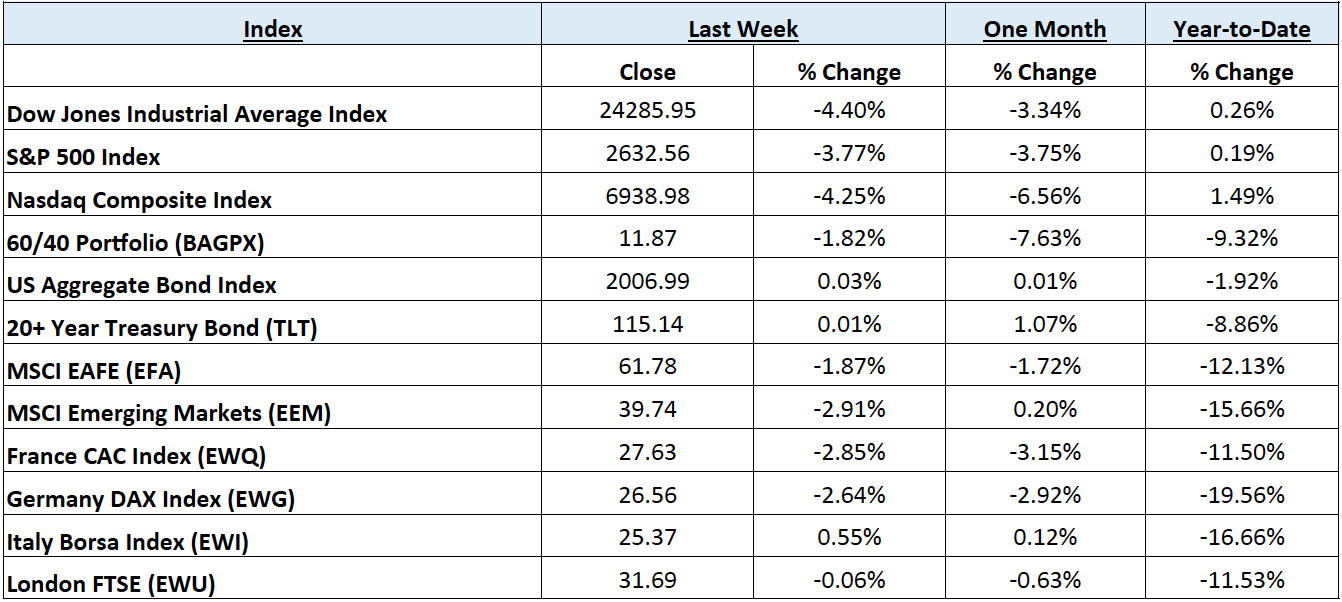

Taking a comprehensive look at the overall current stock market

Taking a comprehensive look at the overall current stock market, you can see the chart below representing eight major indices and their returns through the week ending November 23, 2018. In a truly diversified portfolio, the portfolio’s total return is determined by the performance of all of the individual positions in combination – not individually.

So, understanding the combined overall performance of the indices below, simply average the 12 indices to get a better overall picture of the market. The combined average of all 12 indices is -8.77% year to date.

Data Source: Investors FastTrack, Yahoo Finance, Investopedia

Past performance is not a guarantee of future results. This Update is limited to the dissemination of general information pertaining to its investment advisory services and is not suitable for everyone. The information contained herein should not be construed as personalized investment advice. There is no guarantee that the views and opinions expressed in this newsletter will come to pass. Investing in the stock and bond markets involves gains and losses and may not be suitable for all investors. Information presented herein is subject to change without notice. Horter has experienced periods of underperformance in the past and may also in the future. The returns represented herein are total return inclusive of reinvesting all interest and dividends.

The above equity, bond and cash weightings are targets and may not be the exact current weightings in any particular client account. Specifically, there may be cases where accounts hold higher cash levels than stated in these target weightings. This is usually to accommodate account level activity. Furthermore, some variable annuity and variable universal life accounts may not be able to purchase the exact weightings that we are indicating above due to specific product restrictions, limitations, riders, etc. Please refer to your client accounts for more specifics or call your Horter Investment Management, LLC at (513) 984-9933.

Investment advisory services offered through Horter Investment Management, LLC, a SEC-Registered Investment Advisor. Horter Investment Management does not provide legal or tax advice. Investment Advisor Representatives of Horter Investment Management may only conduct business with residents of the states and jurisdictions in which they are properly registered or exempt from registration requirements. Insurance and annuity products are sold separately through Horter Financial Strategies, LLC. Securities transactions for Horter Investment Management clients are placed through TCA by E*TRADE, TD Ameritrade and Nationwide Advisory Solutions.

For additional information about Horter Investment Management, LLC, including fees and services, send for our disclosure statement as set forth on Form ADV from Horter Investment Management, LLC using the contact information herein. Please read the disclosure statement carefully before you invest or send money.

Dow Jones – Week Ending

WEEKLY MARKET SUMMARY

Global Equities: Global equities declined during the holiday-shortened week, with US markets continuing to sell off. The S&P 500 ended the week down nearly 4%, sliding back into correction territory for the second time this year. Technology sector stocks continued to get punished, with the SPDR Technology Sector ETF (XLK) losing over 5%. Energy shares were also battered as oil fell to new lows, exacerbating concerns over slowing global growth. Foreign developed stocks lost around 2% for the week and emerging markets dipped nearly 3%.

Fixed Income: Treasury yields continued to push lower, ending the week at 3.04%, their lowest level since mid-September. European bond yields slid lower after lackluster economic data cast uncertainty over the coming European Central Bank meeting. German 10-Year Bunds ended the week at 0.34%. High yield bonds ended the week lower as spreads continue to widen. The option-adjusted spread on high yield bonds over treasuries rose as high as 4.33%, the widest spread levels since December of 2016. High yield bond mutual funds and ETFs saw modest inflows of $487 million in the weekly period ended November 14th.

Commodities: Oil prices continued to freefall, sliding 7.76% on Friday on a seventh consecutive weekly loss. US West Texas Intermediate (WTI) prices ended the week at $50.39 a barrel, a staggering 34% drop from their October 3rd price of $76.41. With international benchmark Brent Crude now trading under $60, OPEC is widely anticipated to announce supply cuts during the upcoming December 6th meeting.

WEEKLY ECONOMIC SUMMARY

Brexit Ratification: UK and European Union (EU) leaders will convene on Sunday to ratify the terms of the UK’s exit from the EU. The terms are anticipated to be finalized, barring any last-minute developments. Prime Minister Theresa May will then face the more daunting proposition of securing approval for the from the British Parliament in December.

Durable Goods Orders Disappoint: In a sign that the days of rock-solid US economic data may be coming to an end, orders for long-lasting factory goods fell 4.4% in October. Business investment had been strong earlier in the year as tax cuts worked their way through US corporations, resulting in increased investment into machinery and computers, however the stronger dollar and increased tariffs have caused US businesses to hit the brakes and hold off on new purchases. The slip in energy prices has also caused energy-related businesses to reevaluate their capital investment strategies.

3rd Quarter Earnings: In the lead-up to Black Friday, several retailers reported earnings, and the results did not inspire confidence among investors. Target (TGT) shares were punished as much as 15% after missing on earnings and sales, and reporting falling margins on digital orders. Kohl’s (KSS) earnings beat estimates, but investors keyed in on weaker guidance, sending shares down 12%. Discount retailers TJX (TJX) and Ross Stores (ROST) also saw similar declines after issuing cautious guidance for the holiday season. With over 97% of the S&P 500 having reported Q3 earnings, the forward price to earnings (P/E) ratios based on full-year 2019 expected earnings are 10.87 for Emerging Markets (MSCI EM IMI), 12.81 for Developed International (MSCI EAFE), and 16.6 for the S&P 500.

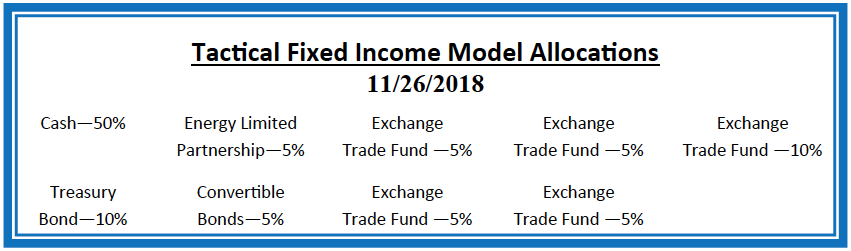

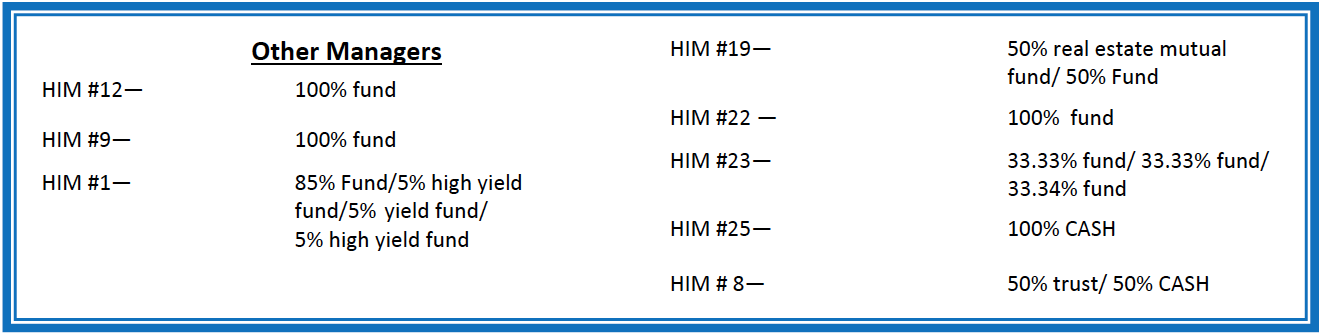

Current Model Allocations

Summary

In utilizing an approach that seeks to limit volatility, it is important to keep perspective of the activity in multiple asset classes. We seek to achieve superior risk-adjusted returns over a full market cycle to a traditional 60% equities / 40% bonds asset allocation. We do this by implementing global mandates of several tactical managers within different risk buckets. For those investors who are unwilling to stomach anything more than minimal downside risk, our goal is to provide a satisfying return over a full market cycle compared to the Barclays Aggregate Bond Index. At Horter Investment Management we realize how confusing the financial markets can be. It is important to keep our clients up to date on what it all means, especially with how it relates to our private wealth managers and their models. We are now in year nine of the most recent bull market, one of

the longest bull markets in U.S. history. At this late stage of the market cycle, it is extremely common for hedged managers to underperform, as they are seeking to limit risk. While none of us know when a market correction will come, even though the movement and volatility sure are starting to act like a correction, our managers have been hired based on our belief that they can accomplish a satisfying return over a full market cycle, — while limiting risk in comparison to a traditional asset allocation approach. At Horter we continue to monitor all of the markets and how our managers are actively managing their portfolios. We remind you there are opportunities to consider with all of our managers. Hopefully this recent market commentary is helpful and thanks for your continued trust and loyalty.