HORTER INVESTMENT MANAGEMENT, LLC

Weekly Commentary horterinvestment.com March 18, 2019

Gundlach: We Are on the Road to a Large Debt Problem

At 1:30pm ET on March 13, the next-to-last paragraph was corrected to read, “Approximately 55% of BBB-rated bonds…” It previously read, “Approximately 55% of high-yield bonds…”

When Donald Trump was campaigning, he said he would eliminate the national debt in eight years. But it has increased by $2 trillion in the first two years of his presidency, leading Jeffrey Gundlach to conclude that we are “on the road to a large debt problem.”

Gundlach is the founder and chief investment officer of Los Angeles-based DoubleLine Capital. He spoke via a webcast with investors on March 12. His talk was titled, “Highway to Hell,” and the focus was on his firm’s flagship mutual fund, the DoubleLine Total Return Fund (DBLTX). The slides from his presentation are available here.

Highway to Hell is a 1979 song from the rock group AC/DC. Gundlach said it illustrates the perdition that awaits the U.S. economy if policymakers continue to allow an unchecked growth of federal deficits.

Recession Watch: Data Worsening

Investors are anxious about the chances of a recession right now. While the Fed doesn’t seem likely to hike us into one any longer, economic fundamentals have just begun to show cracks. It started with housing, then job growth for February, and now it is jobless claims. Jobless claims rose by 6,000 last week after a long stretch of falling numbers. Weekly numbers are seen as less reliable than monthly figures because of random gyrations, but the data could indicate the economy is starting to soften.

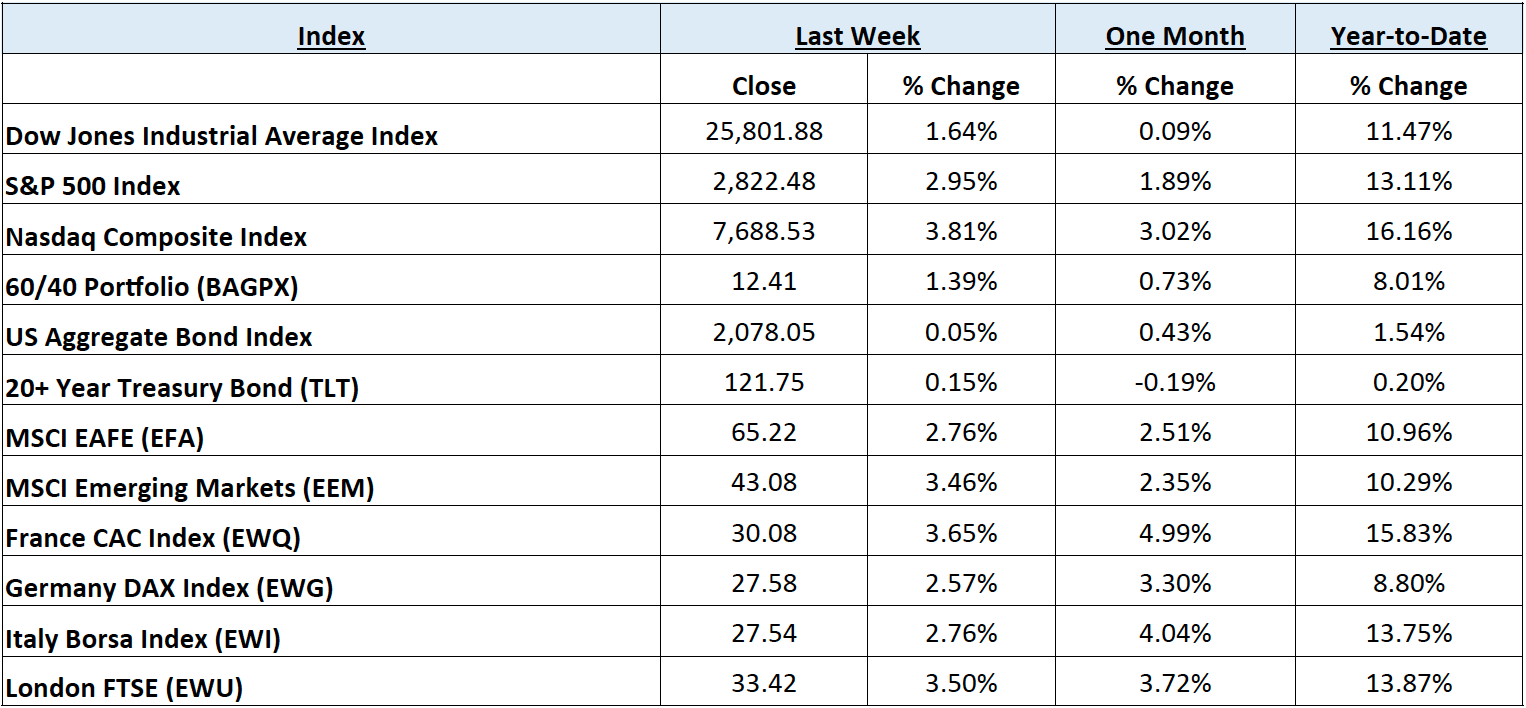

Taking a comprehensive look at the overall current stock market

Taking a comprehensive look at the overall current stock market, you can see the chart below representing eight major indices and their returns through the week ending March 15, 2019. In a truly diversified portfolio, the portfolio’s total return is determined by the performance of all of the individual positions in combination – not individually.

So, understanding the combined overall performance of the indices below, simply average the 12 indices to get a better overall picture of the market. The combined average of all 12 indices is 10.33% year to date.

Data Source: Investors FastTrack, Yahoo Finance, Investopedia

Past performance is not a guarantee of future results. This Update is limited to the dissemination of general information pertaining to its investment advisory services and is not suitable for everyone. The information contained herein should not be construed as personalized investment advice. There is no guarantee that the views and opinions expressed in this newsletter will come to pass. Investing in the stock and bond markets involves gains and losses and may not be suitable for all investors. Information presented herein is subject to change without notice. Horter has experienced periods of underperformance in the past and may also in the future. The returns represented herein are total return inclusive of reinvesting all interest and dividends.

The above equity, bond and cash weightings are targets and may not be the exact current weightings in any particular client account. Specifically, there may be cases where accounts hold higher cash levels than stated in these target weightings. This is usually to accommodate account level activity. Furthermore, some variable annuity and variable universal life accounts may not be able to purchase the exact weightings that we are indicating above due to specific product restrictions, limitations, riders, etc. Please refer to your client accounts for more specifics or call your Horter Investment Management, LLC at (513) 984-9933.

Investment advisory services offered through Horter Investment Management, LLC, a SEC-Registered Investment Advisor. Horter Investment Management does not provide legal or tax advice. Investment Advisor Representatives of Horter Investment Management may only conduct business with residents of the states and jurisdictions in which they are properly registered or exempt from registration requirements. Insurance and annuity products are sold separately through Horter Financial Strategies, LLC. Securities transactions for Horter Investment Management clients are placed through E*TRADE Advisor Services, TD Ameritrade and Nationwide Advisory Solutions.

For additional information about Horter Investment Management, LLC, including fees and services, send for our disclosure statement as set forth on Form ADV from Horter Investment Management, LLC using the contact information herein. Please read the disclosure statement carefully before you invest or send money.

Dow Jones – Week Ending

WEEKLY MARKET SUMMARY

Global Equities: The release of subdued US inflation data helped US equity markets grind higher during the week, signaling that the Federal Reserve would be able to continue its patient policy stance with regards to interest rates. The Technology sector outperformed, helping the Nasdaq Composite Index to lead the major US indices by a healthy margin, gaining 3.82% on the week. The S&P 500 Index rose 2.95% while the Dow Jones Industrial Average, up only 1.64%, was weighed down heavily by the Boeing Company (BA), who had another horrific crash of its new 737 Max 8 aircraft. News of the British Parliament removing the possibility of a hard Brexit, and rising confidence in Chinese policy measures to prevent a hard landing led to solid returns for International equities. Developed International stocks represented by the iShares MSCI EAFE Index Fund ETF (EFA) gained 2.76%, while Emerging Markets represented by the iShares MSCI Emerging Market Index ETF (EEM) gained 3.46% during the week.

Fixed Income: Muted domestic inflation also led to the unusual dynamic of Treasury bonds rising alongside equities. The yield on the 10-year US Treasury Note broke and closed the week below 2.60%, while the German 10-year Bund yield rose .07% to .086%. However, the US Treasury yield curve slumped ominously further, with intermediate 2, 3, and 5-year maturities all yielding less than bills with 1-year to maturity. High yield bond spreads narrowed significantly during the week, back near 3.80%, as the iShares IBoxx High Yield Corporate Bond ETF (HYG) rose .80%. Lipper reported net inflow into high yield funds of $1.04 billion for the week ended 3/13.

Commodities: Oil prices rose with global equity strength, despite reports of robust inventories and slightly relaxed production cuts from weekly OPEC reports. The West Texas Intermediate (WTI) benchmark rose over 4%, to $58.42 per barrel, while the International Brent crude benchmark rose by only 2%, to $67 per barrel. Natural gas prices pulled back by about 2.5%, to $2.79/MMBtu, on reports of record amounts of increased production in 2018 and the effect of the official confirmation of the end of heating season.

WEEKLY ECONOMIC SUMMARY

Consumer Price Index (CPI): The headline CPI measure of inflation rose .2% during the month of February, the first month-on-month (MoM) increase since October ‘18. The year-on-year (YoY) increase of 1.5% matched consensus estimates, but was the smallest increase since September of 2016 thanks inpart to softness in home price appreciation. Contributing to the MoM increase, were prices of apparel, food, gasoline, electricity, and natural gas. The Core CPI, which removes changes for food and energy, was slightly below consensus estimates despite increasing .1% MoM and 2.1% YoY. Decreasing prices for recreation, medical care, and vehicles contributed to the miss.

Durable Goods Orders: January orders for durable goods increased at a better than expected .4% MoM, thanks to a jump in the volatile aircraft orders reading. This may reverse in future readings due to the situation with Boeing (BA). However, when excluding the effect of aircraft and other transportation equipment, the index fell -.1% for the month, missing expectations for a slight increase. Core capital goods (non-defense, non-aircraft), however, rose a surprising .8% thanks to a rebound in orders for machinery, electrical equipment, and communication equipment.

Consumer Sentiment: The preliminary University of Michigan Consumer Confidence survey rebounded this month, after slipping on effects of the government shutdown. The measure of 97.8 significantly outpaced the expected 95.2 and the prior reading of 93.8 with readings for current conditions and expectations rising strongly. The inflation expectations component, closely watched by the Federal Reserve when forming policy, displayed conflicting views with lower expectations for the year ahead, but a higher expectation 5 years on

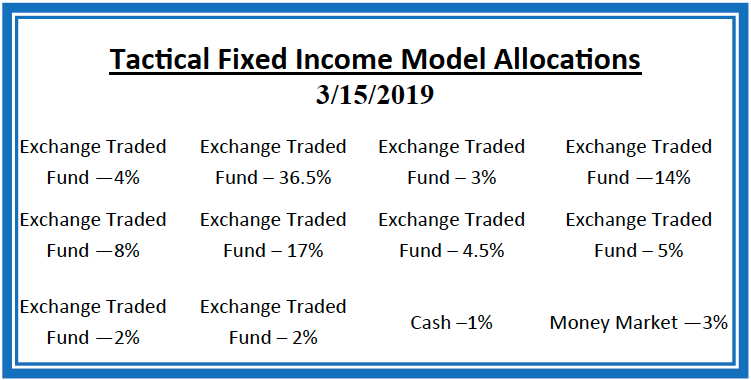

Current Model Allocations

Data Source: Hanlon Investment Management

Summary

In utilizing an approach that seeks to limit volatility, it is important to keep perspective of the activity in multiple asset classes. We seek to achieve superior risk-adjusted returns over a full market cycle to a traditional 60% equities / 40% bonds asset allocation. We do this by implementing global mandates of several tactical managers within different risk buckets. For those investors who are unwilling to stomach anything more than minimal downside risk, our goal is to provide a satisfying return over a full market cycle compared to the Barclays Aggregate Bond Index. At Horter Investment Management we realize how confusing the financial markets can be. It is important to keep our clients up to date on what it all means, especially with how it relates to our private wealth managers and their models. We are now in year nine of the most recent bull market, one of

the longest bull markets in U.S. history. At this late stage of the market cycle, it is extremely common for hedged managers to underperform, as they are seeking to limit risk. While none of us know when a market correction will come, even though the movement and volatility sure are starting to act like a correction, our managers have been hired based on our belief that they can accomplish a satisfying return over a full market cycle, – while limiting risk in comparison to a traditional asset allocation approach. At Horter we continue to monitor all of the markets and how our managers are actively managing their portfolios. We remind you there are opportunities to consider with all of our managers. Hopefully this recent market commentary is helpful and thanks for your continued trust and loyalty.

Data Source: Hanlon Investment Management