HORTER INVESTMENT MANAGEMENT, LLC

Weekly Commentary horterinvestment.com March 5, 2018

No, Worst Probably Not Over Yet for S&P 500, These Analysts Say

Should U.S. stocks keep going at the pace of the past two days, they’ll hit a record before the weekend. But a few Wall Street analysts say pain in equities probably isn’t over yet.

For one, look at history. From 1992 through January, there were four instances when convulsions like this month’s pushed the 10-week rate of change in volatility to an extreme level, according to Canaccord Genuity’s Tony Dwyer. The S&P 500 Index gained on average 5.6 percent after the instances, according to the firm’s data that exclude the market jitters of 2008. Each time, stocks caved in again after the rebound.

The S&P 500 is up 4.9 percent since a 116 percent spike in volatility pushed the rate of volatility’s change to 125 on Canaccord’s rating scale, in the extreme territory.

“The comfort of the rebound should soon fade, either from fear of the Fed, disappointing data, or some combination of the two,” Dwyer said on Monday. “Last week did very little to change our expectation for a potential retest of the ‘shock drop’ low, followed by a very choppy few months that should set the stage for a secondhalf ramp.”

Another issue is the number of stocks changing hands during the rebound. Equities in the New York Stock Exchange Composite Index have gained 5.9 percent since Feb. 8, but their trading volume has been gradually falling to just half of what it was during the rebound’s early days.

Choppiness is here to stay. Margin calls with historic margin debt will increase volatility. —Drew

Bill Gates says it’s ‘a certainty’ that we will have another financial crisis like in 2008

Many economists consider the financial crisis of 2008 to be the worst economic downturn since the Great Depression.

According to Bill Gates, the US is heading toward another one just like it.

On Tuesday, the Microsoft founder held an “Ask Me Anything” event on Reddit. When a user asked, “Do you think in the near future, we will have another financial crisis similar to the one in 2008?” Gates replied with a stern — but still optimistic — warning.

“Yes. It is hard to say when but this is a certainty,” Gates said. “Fortunately we got through that one reasonably well.”

Taking a comprehensive look at the overall current stock market

Taking a comprehensive look at the overall current stock market, you can see the chart below representing eight major indices and their returns through the week ending March 2, 2018. In a truly diversified portfolio, the portfolio’s total return is determined by the performance of all of the individual positions in combination – not individually.

So, understanding the combined overall performance of the indices below, simply average the 7 indices to get a better overall picture of the market. The combined average of all 7 indices is –0.70% year to date.

Past performance is not a guarantee of future results. This Update is limited to the dissemination of general information pertaining to its investment advisory services and is not suitable for everyone. The information contained herein should not be construed as personalized investment advice. There is no guarantee that the views and opinions expressed in this newsletter will come to pass. Investing in the stock and bond markets involves gains and losses and may not be suitable for all investors. Information presented herein is subject to change without notice. Horter has experienced periods of underperformance in the past and may also in the future. The returns represented herein are total return inclusive of reinvesting all interest and dividends.

The above equity, bond and cash weightings are targets and may not be the exact current weightings in any particular client account. Specifically, there may be cases where accounts hold higher cash levels than stated in these target weightings. This is usually to accommodate account level activity. Furthermore, some variable annuity and variable universal life accounts may not be able to purchase the exact weightings that we are indicating above due to specific product restrictions, limitations, riders, etc. Please refer to your client accounts for more specifics or call your Horter Investment Management, LLC at (513) 984-9933.

Investment advisory services offered through Horter Investment Management, LLC, a SEC-Registered Investment Advisor. Horter Investment Management does not provide legal or tax advice. Investment Advisor Representatives of Horter Investment Management may only conduct business with residents of the states and jurisdictions in which they are properly registered or exempt from registration requirements. Insurance and annuity products are sold separately. Securities transactions for Horter Investment Management clients are placed through Trust Company of America, TD Ameritrade and Jefferson National Life Insurance Company.

For additional information about Horter Investment Management, LLC, including fees and services, send for our disclosure statement as set forth on Form ADV from Horter Investment Management, LLC using the contact information herein. Please read the disclosure statement carefully before you invest or send money.

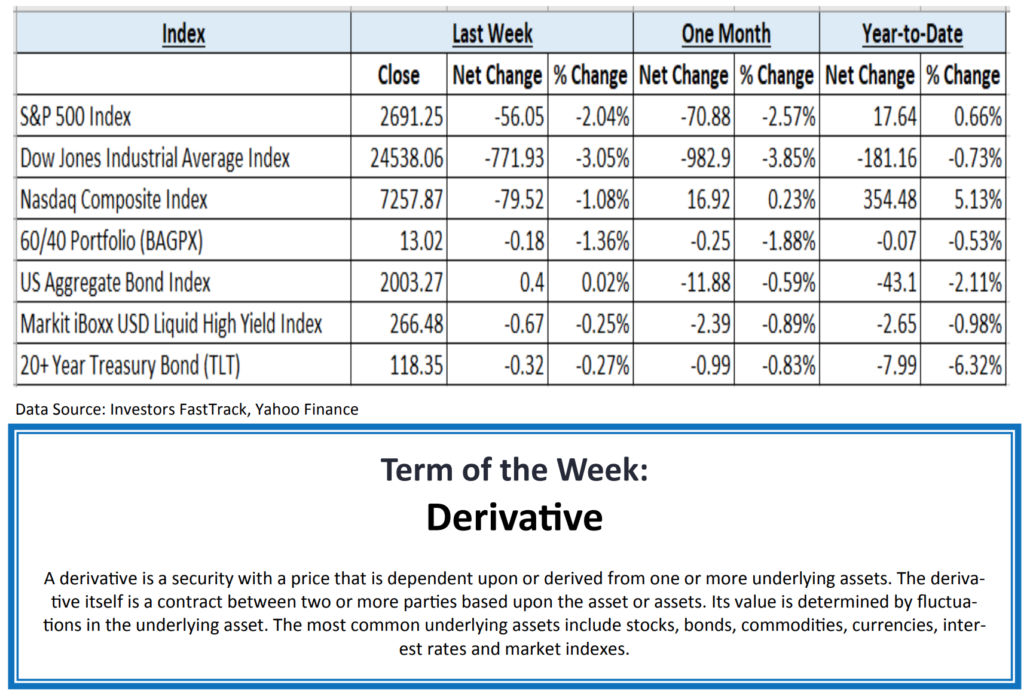

Dow Jones – Week Ending

WEEKLY MARKET SUMMARY

Global Equities: US equity indices ended the week with losses as markets tried to digest protectionist rhetoric from President Trump and hawkish comments from Federal Reserve (Fed) Chair Jerome Powell. The announcement that the US would impose tariffs on imported steel and aluminum drew backlash from other world leaders and has increased the likelihood of igniting a trade war with widespread implications for many industries. The Dow Jones Industrial Average, S&P 500, and Nasdaq indices all closed in the red. Developed International and Emerging market equities also sold off significantly in weekly trading.

Fixed Income: Bond markets were volatile once again as new Fed Chair Jerome Powell spent two days answering questions on Capitol Hill. Investors were hanging on every word, which led to a day one interpretation that four fed rate hikes were appropriate because the economy is stronger now than when the Fed had agreed to three. Powell seemed to be more deliberate with his words on day two of his testimony, because 10-year Treasury yields receded from mid-week highs to close the week little changed at 2.86%. High yield spreads initially tightened to begin the week, but widened to close out the week unchanged with modest outflows from high yield funds.

Commodities: A surge in North American crude output and a general risk-off attitude from the aforementioned tariffs contributed to lower crude oil prices during weekly trading. The US Energy Information Administration (EIA) reported that crude oil inventories increased by three million barrels for the week ending February 23 as the International Brent Crude and the West Texas Intermediate (WTI) benchmarks closed the week down around 4% to $64.53 and $61.42, respectively. The EIA natural gas storage report drawdown helped natural gas prices increase for the week to $2.71 per million British thermal units.

WEEKLY ECONOMIC SUMMARY

Durable Goods Orders: New orders for US-manufactured durable goods fell 3.7% for the month of January. This US Census Bureau leading indicator showed a slowdown in future business spending on goods ranging from small appliances to airplanes. The closely watched core component, which excludes defense spending and aircraft, expressed a soft start to 2018 while dropping for the second straight month for the first time since mid-2016.

S&P Corelogic Case-Shiller HPI: Indicating continued growth, the 20-city Home Price Index released by S&P Dow Jones rose 0.6% month-on-month (MoM) for December. The monthly increase was dominated by western cities including Seattle, Denver, San Francisco, and Las Vegas. Seattle had the largest year-on-year (YoY) increase of 12.7%, with the full 20-city index up a relatively modest 6.3% for the year. Home prices continue to outpace the rate of inflation as rising mortgage rates have not yet dampened demand.

Jobless Claims: The weekly report for new jobless claims came in at the lowest reading in nearly five decades. Far below the consensus range of 226K to 240K, the 210K new claims report indicates strong demand for labor in a US economy that is running at full employment. This tight labor market threatens to turn into a labor shortage that some regions and industries have already started to experience. If a shortage becomes widespread, it would hurt economic growth and increase prices to consumers in the form of rising inflation.

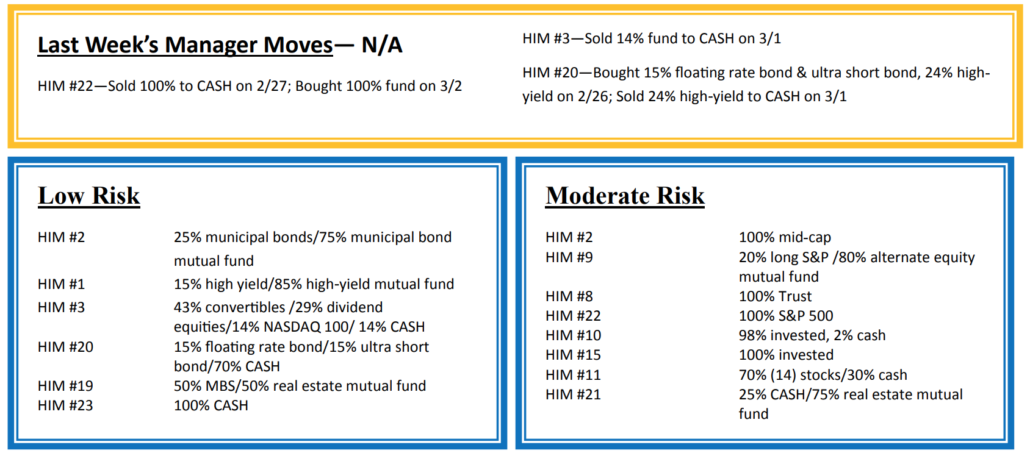

Current Model Allocations

Summary

In utilizing an approach that seeks to limit volatility, it is important to keep perspective of the activity in multiple asset classes. We seek to achieve superior risk-adjusted returns over a full market cycle to a traditional 60% equities / 40% bonds asset allocation. We do this by implementing global mandates of several tactical managers within different risk buckets. For those investors who are unwilling to stomach anything more than minimal downside risk, our goal is to provide a satisfying return over a full market cycle compared to the Barclays Aggregate Bond Index. At Horter Investment Management we realize how confusing the financial markets can be. It is important to keep our clients up to date on what it all means, especially with how it relates to our private wealth managers and their models. We are now in year nine of the most recent bull market, one of the longest bull markets in U.S. history. At this late stage of the market cycle, it is extremely common for hedged managers to underperform, as they are seeking to limit risk. While none of us know when a market correction will come, even though the movement and volatility sure are starting to act like a correction, our managers have been hired based on our belief that they can accomplish a satisfying return over a full market cycle, — while limiting risk in comparison to a traditional asset allocation approach. At Horter we continue to monitor all of the markets and how our managers are actively managing their portfolios. We remind you there are opportunities to consider with all of our managers. Hopefully this recent market commentary is helpful and thanks for your continued trust and loyalty.