HORTER INVESTMENT MANAGEMENT, LLC

Weekly Commentary horterinvestment.com March 26, 2018

Goldman Sees ‘Financial Fragility’ Rising in Markets

Markets are becoming their own worst enemies, according to Gold-man Sachs Group Inc.

The stock-market rout in early February that caused a spike in the Cboe Volatility Index is a symptom of growing “financial fragility,” or big swings in prices caused by breakdowns in markets themselves as opposed to changes in fundamentals, an economist at the bank wrote Monday in a note to clients. To make matters worse, Gold-man says there’s reason to be concerned about liquidity drying up during periods when markets are distressed.

“Future liquidity disruptions may amplify price declines when the current cycle turns,” wrote Charles Himmelberg, Goldman’s co-chief markets economist. “Trading liquidity may be worse than it looks because trading volume in many major markets is increasingly dominated by more speed and less capital.”

The warning on fragility came days after the bank said in a note Friday that investors need to get used to lackluster returns as volatility picks up and stocks and bonds move more in tandem with each other. The selloff in U.S. technology stocks Monday sent the VIX futures curve into backwardation, a telltale sign that the market is under stress, as near-term contracts became more expensive than longer-dated counterparts.

New regulations and technologies such as computer-driven trading have caused a major change in how liquidity is provided since the financial crisis. Goldman says that while the shift has freed up capital for more efficient uses, it will also reduce liquidity when the cycle turns.

For the first time in the past 35 years we have an overpriced stock market and a rising interest rate market! —Drew

BofA Merrill Lynch Global Research Issues Its 2018 Market Outlook

BofA Merrill Lynch Global Research today issued a bullish macro outlook for 2018, calling for robust global economic growth, steady U.S. expansion and solid stock returns that peak in the first half of the year. However, it warns of signs that the long bull market run is nearing the end of its leash, triggering a mid-year pullback along-side potential for some of the best returns in the last gasps of the cycle.

The Research team forecasts modest returns in equities and credit, negative bond returns, a stronger dollar, higher levels of volatility and tighter credit spreads in 2018. Inflation is expected to be the big story of the year, particularly in the U.S., where the labor mar-ket is expected to further tighten and inflation pressures are build-ing. Passage of U.S. tax reform is the main upside risk to economic growth, with far-reaching effects, particularly for emerging mar-kets, that have not been fully priced into the market.

Taking a comprehensive look at the overall current stock market

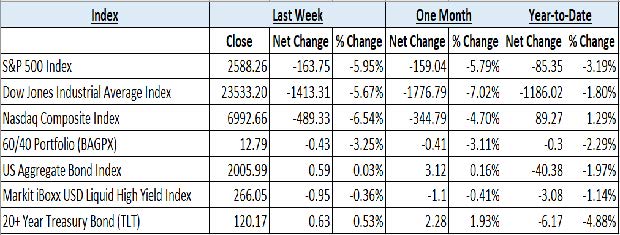

Taking a comprehensive look at the overall current stock market, you can see the chart below representing eight major in-dices and their returns through the week ending March 23, 2018. In a truly diversified portfolio, the portfolio’s total return is determined by the performance of all of the individual positions in combination – not individually.

So, understanding the combined overall performance of the indices below, simply average the 7 indices to get a better overall picture of the market. The combined average of all 7 indices is –2.00% year to date.

Data Source: Investors FastTrack, Yahoo Finance

Past performance is not a guarantee of future results. This Update is limited to the dissemination of general information pertaining to its investment advisory services and is not suitable for everyone. The information contained herein should not be construed as personalized investment advice. There is no guarantee that the views and opinions expressed in this newsletter will come to pass. Investing in the stock and bond markets involves gains and losses and may not be suitable for all investors. Information pre-sented herein is subject to change without notice. Horter has experienced periods of underperformance in the past and may also in the future. The returns represented herein are total return inclusive of reinvesting all interest and dividends.

The above equity, bond and cash weightings are targets and may not be the exact current weightings in any particular client account. Specifically, there may be cases where accounts hold higher cash levels than stated in these target weightings. This is usually to accommodate account level activity. Furthermore, some variable annuity and varia-ble universal life accounts may not be able to purchase the exact weightings that we are indicating above due to specific product restrictions, limitations, riders, etc. Please refer to your client accounts for more specifics or call your Horter Investment Management, LLC at (513) 984-9933.

Investment advisory services offered through Horter Investment Management, LLC, a SEC-Registered Investment Advisor. Horter Investment Management does not provide legal or tax advice. Investment Advisor Representatives of Horter Investment Management may only conduct business with residents of the states and jurisdictions in which they are properly registered or exempt from registration requirements. Insurance and annuity products are sold separately. Securities transactions for Horter Investment Management clients are placed through Trust Company of America, TD Ameritrade and Jefferson National Life Insurance Company.

For additional information about Horter Investment Management, LLC, including fees and services, send for our disclosure statement as set forth on Form ADV from Horter Investment Management, LLC using the contact information herein. Please read the disclosure statement carefully before you invest or send money.

Dow Jones – Week Ending

WEEKLY MARKET SUMMARY

Global Equities: Goldilocks economic news was not enough to save US and world equities from the intensifying trade war rhetoric between the Trump administration and China. Tariffs on $60 billion in US imports from China because of unfair trade practices and theft of intellectual property were countered by levies on US goods ranging from aluminum to pork and wine. The S&P 500 closed down over 5% for the week, while the Nasdaq Composite Index fared even worse with the high-flying Technology sector falling back to Earth. International equities were not spared from the carnage with Emerging Markets lagging their Developed brethren.

Fixed Income: The 10-Year US Treasury yield crept higher to begin the week above 2.9% in anticipation of the Federal Reserve (Fed) Open Market Committee meeting. With no new hawkish information from the Fed statement or the following testimony by Fed Chair Jerome Powell, the benchmark rate fell back down to 2.81% to close out the week as a flight to safety precipitated from the volatile equity market. High yield bond spreads widened slightly while the corresponding funds saw continued outflows.

Commodities: Oil prices had a nice week, somewhat symbolically, as Saudi Crown Prince Mohammed bin Salman was in the US for a meeting with President Trump. The outlook for Middle-East turmoil, the appointment of “Iran hawk” John Bolton as National Security Advisor, and a Saudi announcement of OPEC oil cuts extend-ing into 2019, all combined for an excellent tailwind to prices. The International Brent Crude oil contract was up 6.5% to $70.46 per barrel, with the US benchmark West Texas Intermediate up 5.7% to $65.91 per barrel.

WEEKLY ECONOMIC SUMMARY

Jobless Claims: Another strong jobs report was released on Thursday indicating only a slight increase of the amount of new claims. The 229K number of new claims shows that employers are holding on to workers like never before, with the 4-week moving average of only 223.75K. Claims have now been below the 300K threshold for 159 straight weeks, which is the longest streak since 1970 when the labor market was obviously much smaller.

PMI Composite Flash: The Purchasing Managers Index (PMI) Composite of 54.3 was very strong despite coming in below consensus expectations of 55.2. The real surprise of the survey of around 1,000 service manufacturing and service sector companies was the fantastic manufacturing PMI, which is equal to a three-year high. Overshadowing a slumping services number, manufacturing orders, production, and employment all showed excellent strength. Unfortunately, a key theme of the survey was inflationary pricing pressure. Factory costs showed the largest jump in seven years which will no doubt be passed on to customers, with average prices charged for goods also rising at a strong clip.

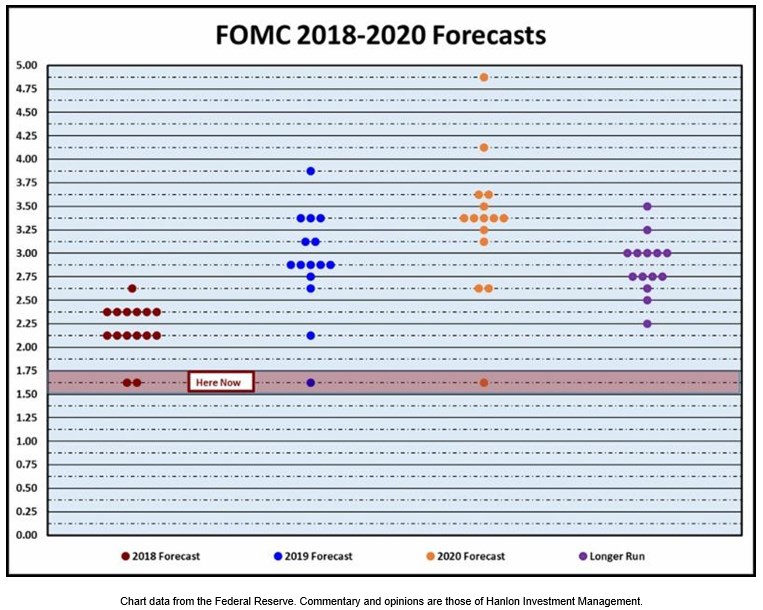

FOMC Announcement: The first meeting for new Fed Chair Je-rome Powell went as planned with a .25% rate hike of the bench-mark Federal Funds rate to 1.5-1.75%. “Moderation” is the key theme with the inflation target unchanged from prior announcements. With a strong labor market, yet household spending and fixed investment being described as moderated, the Fed is predict-ed to stay on course for three total rate hikes this year. The door is left open for a possible fourth hike, as an equal amount of Fed governors plotted their dots one notch above the previously pre-scribed rate to end 2018.

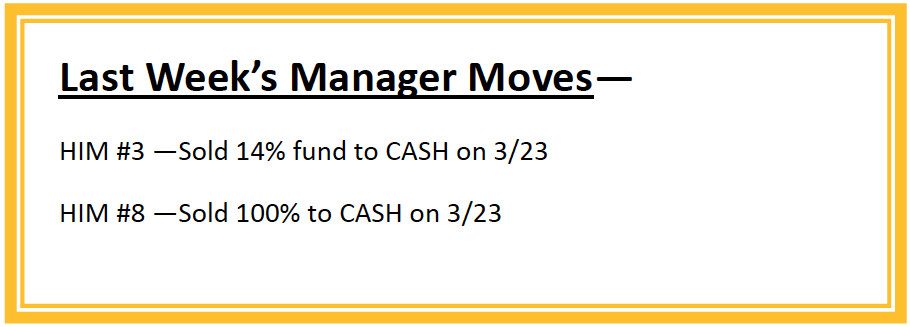

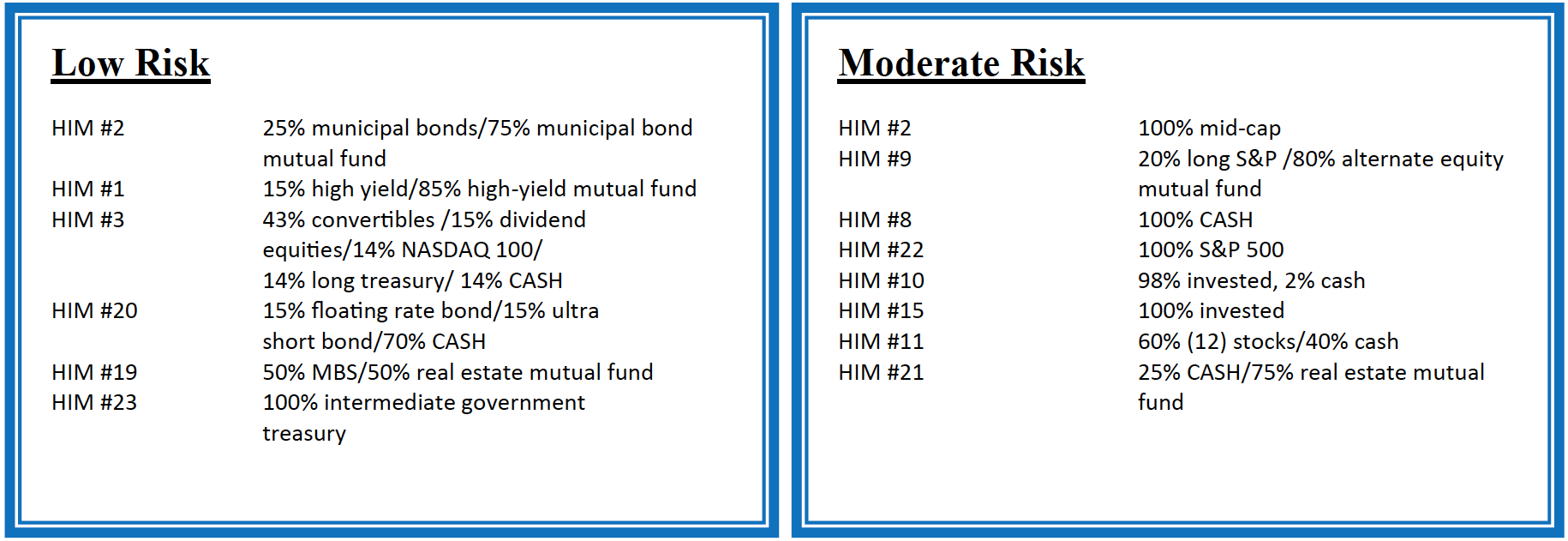

Current Model Allocations

Summary

In utilizing an approach that seeks to limit volatility, it is important to keep perspective of the activity in multiple asset classes. We seek to achieve superior risk-adjusted returns over a full market cycle to a traditional 60% equities / 40% bonds asset allocation. We do this by implementing global mandates of several tactical managers with-in different risk buckets. For those investors who are unwilling to stomach anything more than minimal downside risk, our goal is to provide a satisfying return over a full market cycle compared to the Barclays Aggregate Bond Index. At Horter Investment Management we realize how confusing the financial markets can be. It is important to keep our clients up to date on what it all means, especially with how it relates to our private wealth managers and their mod-els. We are now in year nine of the most recent bull market, one of

the longest bull markets in U.S. history. At this late stage of the mar-ket cycle, it is extremely common for hedged managers to underperform, as they are seeking to limit risk. While none of us know when a market correction will come, even though the movement and volatility sure are starting to act like a correction, our managers have been hired based on our belief that they can accomplish a satisfying return over a full market cycle, — while limiting risk in comparison to a traditional asset allocation approach. At Horter we continue to monitor all of the markets and how our managers are actively man-aging their portfolios. We remind you there are opportunities to consider with all of our managers. Hopefully this recent market commentary is helpful and thanks for your continued trust and loyalty.