HORTER INVESTMENT MANAGEMENT, LLC

Weekly Commentary horterinvestment.com March 19, 2018

Gundlach Sees Bull Market Over If 10-Yr. Treasury Tops 3%

Jeffrey Gundlach thinks that 2018 will be a down year for equities, with a negative S&P 500 return.

In a Tuesday webcast entitled “Inflation is Inflationary,” Gundlach, CIO of DoubleLine Capital, reiterated his conviction that risk assets will suffer in 2018, but dismissed the idea that a recession was immi-nent.

“It seems to me that we are going to have a negative rate of return on the S&P 500 this year, and my conviction on that is pretty high—higher than my conviction on whether bond yields break to the up-side or the downside,” said Gundlach, who added that 10-year Treasury yields should break to the upside.

Gundlach predicted that if the 10-year Treasury yield reaches 3 per-cent, the nine-year bull market will come to an end. Such a move would increase his conviction that the S&P 500 will end 2018 in the red.

The 10-year U.S. Treasury has hovered over 2.8 for several weeks, a rise that coincided with volatility in equity markets.

“This is shaping up to be a very different year from the one that just passed in 2017,” said Gundlach. “We no longer have non-volatile markets. We’ve moved into a regime of volatility.”

Gundlach offered five indicators that suggest a recession is not likely in the near term: rising leading economic indicators, expanding manufacturing production, stable real GDP, stable business and con-sumer sentiment and stable high-yield spreads.

Is 3% on the 10 Year US Treasury the “tipping point” for the stock market “to go down”? We will see! —Drew

A Decade After Bear’s Collapse, the Seeds of Instability Are Germinating Again

A big financial-firm collapse in near future is exceedingly unlikely, but another crisis isn’t

Since the bailout of Bear Stearns Cos. a decade ago this week and the failure of Lehman Brothers six months later, regulators have made it their mission to prevent a repeat.

Yet even though a big financial-firm collapse in the near future is exceedingly unlikely, another crisis isn’t. Bear and Lehman were the manifestation of deeper economic forces that since the 1970s have produced crises roughly every decade. They are still at work today: ample flows of capital across borders, mounting debts owed by governments, corporations and households, and ultralow interest rates that nurture risk-taking in hidden corners of the economy.

For a quarter-century after World War II, the world was virtually crisis-free. Widespread defaults during the Great Depression and the war left a relatively debt-free path for economic growth, says Harvard University economist Kenneth Rogoff, co-author with Carmen Reinhart of “This Time is Different: Eight Centuries of Financial Folly.” Capital controls limited how much money could cross borders, while rules such as interest-rate ceilings limited who could borrow and how much.

By the early 1980s, though, deregulation had allowed capital to flow freely within and across borders and crises became a regular oc-currence: the Latin American debt crisis that began in 1982, the U.S. commercial real estate and savings and loan crisis of the 1980s, the Asian and Russian financial crisis of 1997-98, the dot-com bubble of 1998-2000, the U.S. mortgage crisis of 2007-2009 and the Eu-ropean sovereign debt crisis of 2009-2013, interspersed with country-level crises such as in Scandinavia in the early 1990s and Japan throughout that decade.

Huge worldwide debt with rising interest rates is a major problem that could rock the market.—Drew

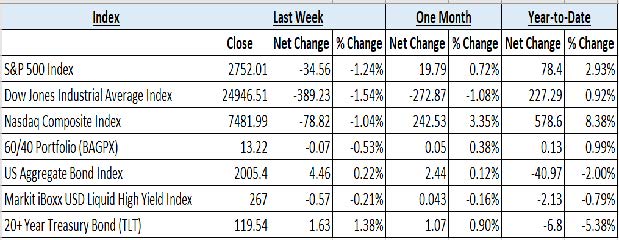

Taking a comprehensive look at the overall current stock market

Taking a comprehensive look at the overall current stock market, you can see the chart below representing eight major in-dices and their returns through the week ending March 9, 2018. In a truly diversified portfolio, the portfolio’s total return is determined by the performance of all of the individual positions in combination – not individually.

So, understanding the combined overall performance of the indices below, simply average the 7 indices to get a better overall picture of the market. The combined average of all 7 indices is 1.05% year to date.

Data Source: Investors FastTrack, Yahoo Finance

Past performance is not a guarantee of future results. This Update is limited to the dissemination of general information pertaining to its investment advisory services and is not suitable for everyone. The information contained herein should not be construed as personalized investment advice. There is no guarantee that the views and opinions expressed in this newsletter will come to pass. Investing in the stock and bond markets involves gains and losses and may not be suitable for all investors. Information pre-sented herein is subject to change without notice. Horter has experienced periods of underperformance in the past and may also in the future. The returns represented herein are total return inclusive of reinvesting all interest and dividends.

The above equity, bond and cash weightings are targets and may not be the exact current weightings in any particular client account. Specifically, there may be cases where accounts hold higher cash levels than stated in these target weightings. This is usually to accommodate account level activity. Furthermore, some variable annuity and varia-ble universal life accounts may not be able to purchase the exact weightings that we are indicating above due to specific product restrictions, limitations, riders, etc. Please refer to your client accounts for more specifics or call your Horter Investment Management, LLC at (513) 984-9933.

Investment advisory services offered through Horter Investment Management, LLC, a SEC-Registered Investment Advisor. Horter Investment Management does not provide legal or tax advice. Investment Advisor Representatives of Horter Investment Management may only conduct business with residents of the states and jurisdictions in which they are properly registered or exempt from registration requirements. Insurance and annuity products are sold separately. Securities transactions for Horter Investment Management clients are placed through Trust Company of America, TD Ameritrade and Jefferson National Life Insurance Company.

For additional information about Horter Investment Management, LLC, including fees and services, send for our disclosure statement as set forth on Form ADV from Horter Investment Management, LLC using the contact information herein. Please read the disclosure statement carefully before you invest or send money.

Dow Jones – Week Ending

WEEKLY MARKET SUMMARY

Global Equities: The steady turnover within the Trump admin-istration continued this week, with the firing of Secretary of State Rex Tillerson. All three major domestic equity indices slipped in weekly trading as investors continued to fret over the possibility of a trade war in response to proposed US tariffs targeting Chinese imports. Among domestic equity sectors, only Utilities ended the week with gains, while Materials fared the worst. Foreign Devel-oped and Emerging Market equities also closed out the week with modest losses.

Fixed Income: The 10-Year US Treasury yield ended the week down slightly at 2.84%. Domestic high yield bond spreads over Treasuries widened from 3.56% to 3.62%. High yield bond mutual funds and ETFs reported very slight inflows of $11 million during the weekly period ended March 14th.

Commodities: Oil prices ended the week relatively unchanged, with domestic West Texas Intermediate trading around $62.33 and international Brent Crude at $66.16 as of Friday afternoon. Oil-sensitive Master Limited Partnerships (MLPs) sold off sharply on Thursday after the Federal Energy Regulatory Commission ruled against provisions that allow some MLPs to recover some taxes within the fees they charge to transport crude.

WEEKLY ECONOMIC SUMMARY

Moderate inflation data: US consumer prices crept higher in Feb-ruary, but the 0.2% month-over-month pace was in line with esti-mates and should not prompt a major response from the Federal Reserve. Producer price inflation was similarly tepid, also rising in line with estimates at 0.2% month over month.

Retail sales weigh on growth estimates: Data showed continued weakness in the Retail sector, with month-over-month retail sales slipping -0.1%, badly missing consensus estimates for a 0.4% gain. It was the third straight month of disappointing data, with US households buying fewer big ticket items such as cars and trucks. Analysts will be watching data closely to see if the tax cuts trickle down to consumers and spur spending in the coming months.

Eurozone QE to continue? Economists and investors have been waiting for the European Central Bank (ECB) to reign in its aggres-sive stimulus policies, however slowing inflation may give ECB President Mario Draghi reason to pause in unwinding the pro-gram. Consumer price data was revised lower and now shows a yearly rise of just 1.1% for February, far from the 2% target im-posed by the ECB. Draghi could call for an extension to the stimu-lus program should inflation data fail to materialize in the coming months.

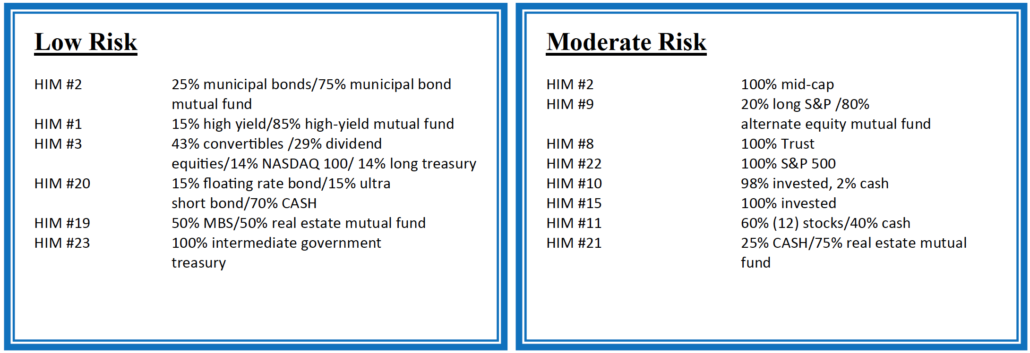

Current Model Allocations

Summary

In utilizing an approach that seeks to limit volatility, it is important to keep perspective of the activity in multiple asset classes. We seek to achieve superior risk-adjusted returns over a full market cycle to a traditional 60% equities / 40% bonds asset allocation. We do this by implementing global mandates of several tactical managers with-in different risk buckets. For those investors who are unwilling to stomach anything more than minimal downside risk, our goal is to provide a satisfying return over a full market cycle compared to the Barclays Aggregate Bond Index. At Horter Investment Management we realize how confusing the financial markets can be. It is im-portant to keep our clients up to date on what it all means, especial-ly with how it relates to our private wealth managers and their mod-els. We are now in year nine of the most recent bull market, one of

the longest bull markets in U.S. history. At this late stage of the mar-ket cycle, it is extremely common for hedged managers to underper-form, as they are seeking to limit risk. While none of us know when a market correction will come, even though the movement and vol-atility sure are starting to act like a correction, our managers have been hired based on our belief that they can accomplish a satisfying return over a full market cycle, — while limiting risk in comparison to a traditional asset allocation approach. At Horter we continue to monitor all of the markets and how our managers are actively man-aging their portfolios. We remind you there are opportunities to consider with all of our managers. Hopefully this recent market commentary is helpful and thanks for your continued trust and loyalty.