HORTER INVESTMENT MANAGEMENT, LLC

Weekly Commentary horterinvestment.com March 12, 2018

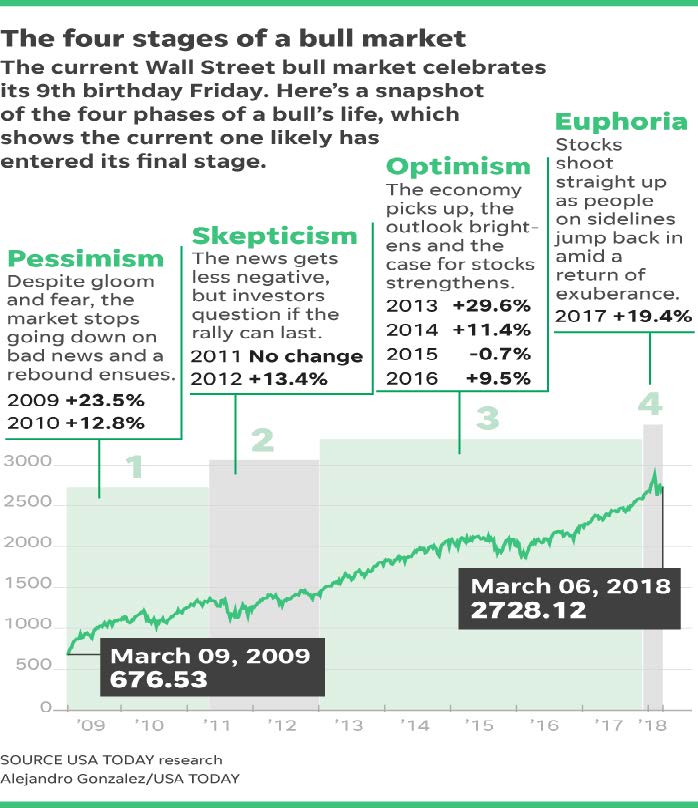

Is the bull market for stocks moving into a more dangerous phase?

“Bull markets are born on pessimism, grown on skepticism, mature on optimism and die on euphoria,” said the late Sir John Templeton, the legendary value investor, laying out the four stages of a bull.

The bull market for stocks, which turns 9 on Friday, is getting up there in age and likely has entered its final phase.

Just as people have life stages, so do financial “bulls,” which are long periods of rising stock prices lasting about five years on average. If you invested in the current one, you’re happy: Putting $100,000 in a broad index fund at the start of the bull on March 9, 2009, and keeping it there would have boosted your investment to $425,000 today.

But know this: Each phase of a bull is distinctive, with unique re-wards and risks for investors, whether they manage a 401(k) or day trade.

“Bull markets are born on pessimism, grown on skepticism, mature on optimism and die on euphoria,” said the late Sir John Templeton, the legendary value investor, laying out the four stages of a bull.

We are definitely in the euphoric stage. Investors should make sure their personal risk score matches the portfolio design. —Drew

‘It could be a deep correction’ — J.P. Morgan co-president warns of 40% stock pullback

Stock traders buckle up — the market is set for as much as a 40% plunge in the next two to three years, essentially wiping out the last two year’s market rally in the U.S.

That’s the warning from J.P. Morgan JPM, +0.25% Co-President Daniel Pinto, who in an interview with Bloomberg Television on Thurs-day said “we know there will be a correction at some point.” A correction is usually defined by a more than 10% drop from a recent market peak.

A 40% plunge would erase the recent gains for U.S. stocks. The S&P 500 SPX, +0.34%has rallied 38% over the past two years, while the Dow Jones Industrial DJIA, +0.39%has soared 45% in that period.

Pinto’s prediction comes as traders already are nervous over the potential fallout from President Donald Trump’s tariffs on steel and aluminum imports.

Trump on Thursday moved ahead with his plans, signing proclamations that will tax steel imports by 25% and aluminum by 10%.

Should Trump, however, expand the trade measures, there’s a risk it could further rattle traders, Pinto said.

A 40 % Drop? If clients don’t have the ability to go risk off to cash, it could be devastating to retirees & pre-retirees —Drew

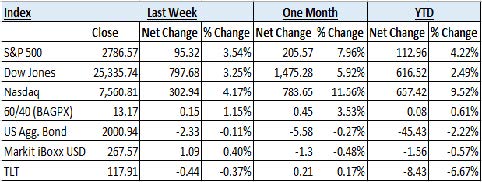

Taking a comprehensive look at the overall current stock market

Taking a comprehensive look at the overall current stock market, you can see the chart below representing eight major in-dices and their returns through the week ending March 9, 2018. In a truly diversified portfolio, the portfolio’s total return is determined by the performance of all of the individual positions in combination – not individually.

So, understanding the combined overall performance of the indices below, simply average the 7 indices to get a better overall picture of the market. The combined average of all 7 indices is 1.05% year to date.

Data Source: Investors FastTrack, Yahoo Finance

Past performance is not a guarantee of future results. This Update is limited to the dissemination of general information pertaining to its investment advisory services and is not suitable for everyone. The information contained herein should not be construed as personalized investment advice. There is no guarantee that the views and opinions expressed in this newsletter will come to pass. Investing in the stock and bond markets involves gains and losses and may not be suitable for all investors. Information pre-sented herein is subject to change without notice. Horter has experienced periods of underperformance in the past and may also in the future. The returns represented herein are total return inclusive of reinvesting all interest and dividends.

The above equity, bond and cash weightings are targets and may not be the exact current weightings in any particular client account. Specifically, there may be cases where accounts hold higher cash levels than stated in these target weightings. This is usually to accommodate account level activity. Furthermore, some variable annuity and varia-ble universal life accounts may not be able to purchase the exact weightings that we are indicating above due to specific product restrictions, limitations, riders, etc. Please refer to your client accounts for more specifics or call your Horter Investment Management, LLC at (513) 984-9933.

Investment advisory services offered through Horter Investment Management, LLC, a SEC-Registered Investment Advisor. Horter Investment Management does not provide legal or tax advice. Investment Advisor Representatives of Horter Investment Management may only conduct business with residents of the states and jurisdictions in which they are properly registered or exempt from registration requirements. Insurance and annuity products are sold separately. Securities transactions for Horter Investment Management clients are placed through Trust Company of America, TD Ameritrade and Jefferson National Life Insurance Company.

For additional information about Horter Investment Management, LLC, including fees and services, send for our disclosure statement as set forth on Form ADV from Horter Investment Management, LLC using the contact information herein. Please read the disclosure statement carefully before you invest or send money.

Dow Jones – Week Ending

WEEKLY MARKET SUMMARY

Global Equities: All three major US equity market indices finished the week with solid gains, with a large chunk of the returns coming Friday after a market-pleasing Employment Situation report. Also, after much speculation, investors received some clarity on the Trump import tariffs that will exclude NAFTA partners Canada and Mexi-co. The tech-heavy Nasdaq Composite continued to outperform the major indices and even made new all-time highs to close out the week. Small-cap equities also performed very well, up over 4% for the week. Emerging and Developed market equities rebounded nicely, nearly reversing all the losses from the tough prior week.

Fixed Income: The 10-Year US Treasury yield was range-bound during weekly trading, bouncing around between 2.85% and 2.91%. Positive economic news caused the benchmark yield to close the week near the high-end of that range at 2.89%. High yield bond funds had posi-tive returns during the week, following the move in equities on Friday. Yield spreads over Treasuries tightened somewhat with small outflows from high yield funds during the week.

Commodities: A rough week for crude oil prices eased with a late week rally due to a toned-down trade war rhetoric and a falling US rig count. An Energy Information Administration (EIA) report of an in-crease in crude oil inventories led to a mid-week slump, but prices showed resilience even with the US dollar holding its ground. Interna-tional Brent Crude and the West Texas Intermediate (WTI) bench-marks closed the week up slightly to $65.55 and $62.05, respective-ly. The sixteenth straight EIA reported weekly drawdown in natural gas storage helped prices increase again for the week to $2.73 per million British thermal units.

WEEKLY ECONOMIC SUMMARY

Beige Book: The Beige Book, released prior to monetary policy meetings by the US Federal Reserve, characterizes regional econom-ic conditions across twelve districts using qualitative information to identify emerging trends otherwise unavailable in economic data. The report indicated “modest to moderate” expansion of economic activi-ty with mixed consumer spending and declining auto sales in all dis-tricts. “Moderate” was a clear theme in the report, as the adjective was also used to describe employment growth, transportation costs, and inflation across districts. This is not a description that would sug-gest a necessary fourth increase for the Fed Funds rate this year.

Employment Situation: The much-anticipated February release of the US employment situation was headlined by a substantial 313,000 month-on-month (MoM) increase in non-farm payrolls. The surprise increase, led by growth in the construction sector, highlighted the robustness of the US labor market and blew away consensus esti-mates. The report, however, also indicated lackluster wage growth and an unemployment rate that remained unchanged from the previ-ous month at 4.1%. Initial market reactions sent the yield on 10-Year US Treasuries above 2.9% temporarily, and had a positive impact on equity markets. The report pleased equity investors as it shows posi-tive signs for the economy without signals for over-heating.

European Central Bank Meeting: During its monetary policy meeting, the European Central Bank (ECB) and its President Mario Draghi decided unsurprisingly to leave rates unchanged and said it will continue its €30 billion per-month bond buying program through Sep-tember. Somewhat surprisingly, prior language about increasing the monetary stimulus if the economic outlook became less favorable was removed from the statement. Viewed as less accommodative, the language removal initially caused the Euro to spike against the US dollar until it was walked back by Draghi. It is unclear if the ECB will end the program abruptly or begin by tapering the amount of pur-chases, but an eventual end to quantitative easing in Europe is on the horizon.

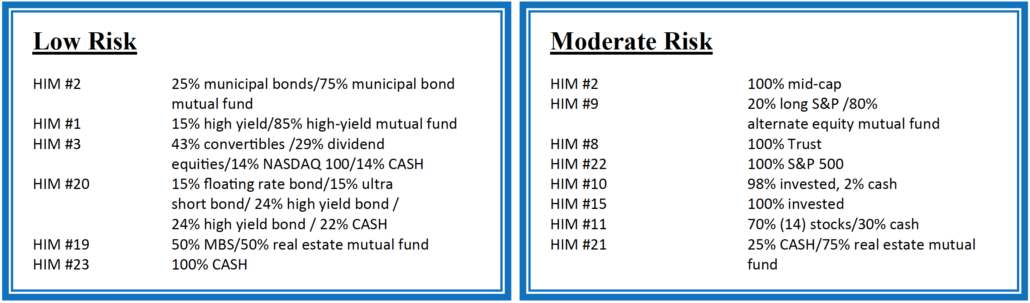

Current Model Allocations

Summary

In utilizing an approach that seeks to limit volatility, it is important to keep perspective of the activity in multiple asset classes. We seek to achieve superior risk-adjusted returns over a full market cycle to a traditional 60% equities / 40% bonds asset allocation. We do this by implementing global mandates of several tactical managers with-in different risk buckets. For those investors who are unwilling to stomach anything more than minimal downside risk, our goal is to provide a satisfying return over a full market cycle compared to the Barclays Aggregate Bond Index. At Horter Investment Management we realize how confusing the financial markets can be. It is im-portant to keep our clients up to date on what it all means, especial-ly with how it relates to our private wealth managers and their mod-els. We are now in year nine of the most recent bull market, one of

the longest bull markets in U.S. history. At this late stage of the mar-ket cycle, it is extremely common for hedged managers to underper-form, as they are seeking to limit risk. While none of us know when a market correction will come, even though the movement and vol-atility sure are starting to act like a correction, our managers have been hired based on our belief that they can accomplish a satisfying return over a full market cycle, — while limiting risk in comparison to a traditional asset allocation approach. At Horter we continue to monitor all of the markets and how our managers are actively man-aging their portfolios. We remind you there are opportunities to consider with all of our managers. Hopefully this recent market commentary is helpful and thanks for your continued trust and loyalty.