HORTER INVESTMENT MANAGEMENT, LLC

Weekly Commentary horterinvestment.com June 18, 2018

Just the Fear of a Trade War is Straining the Global Economy

Only a few months ago, the global economy appeared to be humming, with all major nations growing in unison. Now, the world’s fortunes are imperiled by an unfolding trade war.

As the Trump administration imposes tariffs on allies and rivals alike, provoking broad retaliation, global commerce is suffering disruption, flashing signs of strains that could hamper economic growth. The latest escalation came on Friday, when President Trump announced fresh tariffs on $50 billion in Chinese goods, prompting swift retribution from Beijing.

As the conflict broadens, shipments are slowing at ports and airfreight terminals around the world. Prices for crucial raw materials are rising. At factories from Germany to Mexico, orders are being cut and investments delayed. American farmers are losing sales as trading partners hit back with duties of their own.

Workers in a Canadian steel mill scrambled to recall rail cars headed to the United States border after Mr. Trump this month slapped tariffs on imported metals. A Seattle customer soon canceled an order.

“The impact was felt immediately,” said Jon Hobbs president of AltaSteel in Edmonton. “The penny is really dropping now as to what this means to people’s businesses.”

The Trump administration portrays its confrontational stance as a means of forcing multinational companies to bring factory production back to American shores. Mr. Trump has described trade wars as “easy to win” while vowing to rebalance the United States’ trade deficits with major economies like China and Germany.

Consumer Sentiment Rises to Highest Level in Three Months

Consumer sentiment jumped at the beginning of June, moving opposite of expectations and heading back toward levels seen earlier this year.

The University of Michigan’s Friday report on consumer attitudes about the economy hit 99.3 in a preliminary June reading, higher than the 98.3 expected by a survey of Reuters economists. The index was more than a point above May’s reading of 98 and rose to its highest level since hitting 101.4 in March.

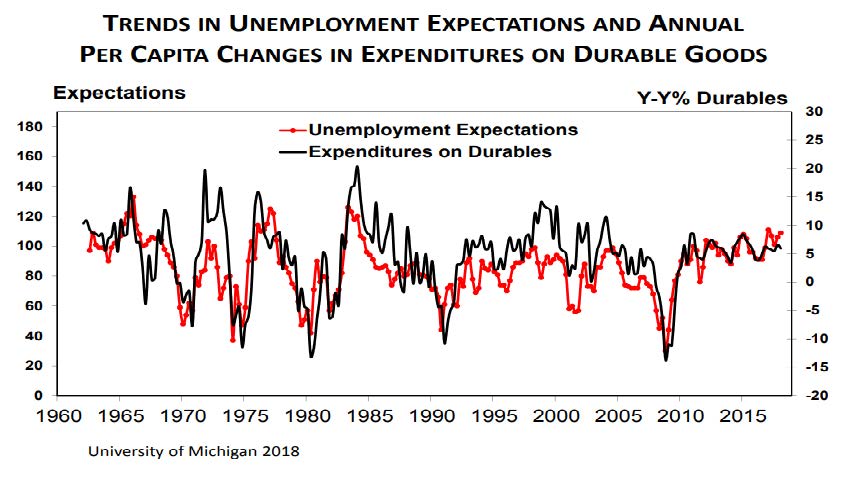

Consumers surveyed by the University of Michigan viewed both their current financial situation and the current buying conditions for household durables more favorably, according to chief economist Richard Curtin.

“Greater certainty about future income and job prospects have become the main drivers of more favorable purchase plans,” Curtin said in a statement.

Curtin highlighted a chart showing the connection between how consumers’ expect unemployment to change and the current yearly per capita change for spending on durable goods.

The chart shows that “the unemployment rate during the year ahead was more often expected to decline than increase,” Curtin said, “which should modestly accelerate purchases.”

The survey measures 500 consumers’ attitudes on future economic prospects, in areas such as personal finances, inflation, unemployment, government policies and interest rates.

Taking a comprehensive look at the overall current stock market

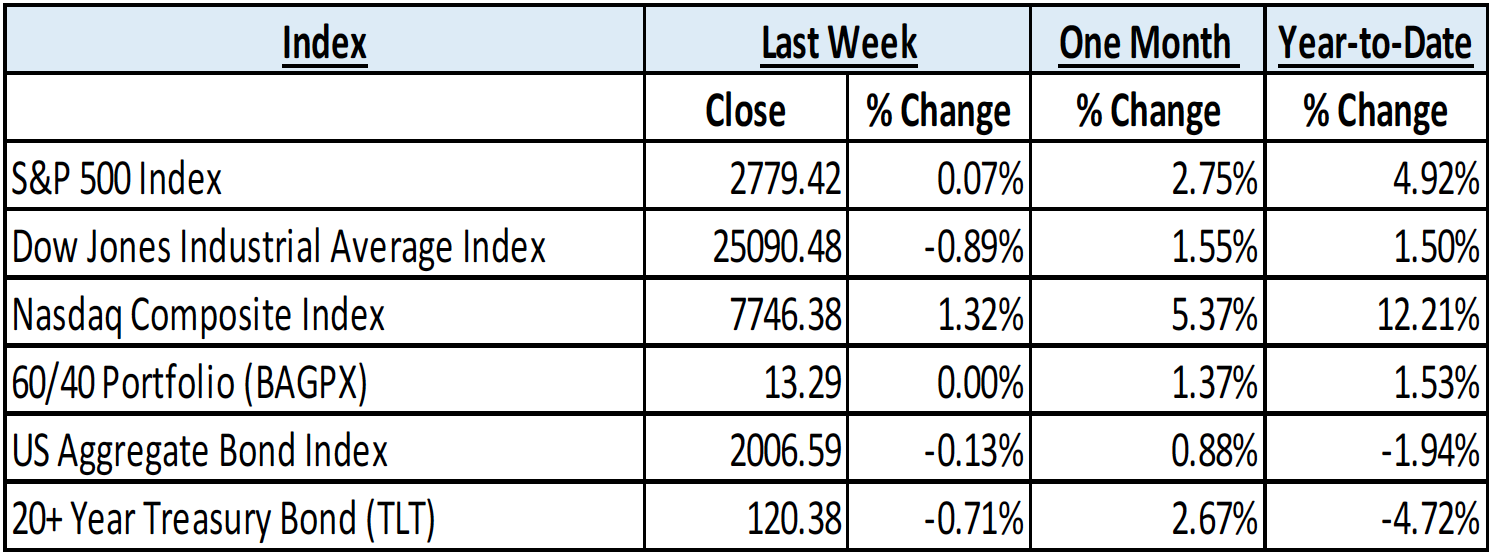

Taking a comprehensive look at the overall current stock market, you can see the chart below representing eight major indices and their returns through the week ending June 18, 2018. In a truly diversified portfolio, the portfolio’s total return is determined by the performance of all of the individual positions in combination – not individually.

So, understanding the combined overall performance of the indices below, simply average the 6 indices to get a better overall picture of the market. The combined average of all 6 indices is 2.25% year to date.

Data Source: Investors FastTrack, Yahoo Finance

Past performance is not a guarantee of future results. This Update is limited to the dissemination of general information pertaining to its investment advisory services and is not suitable for everyone. The information contained herein should not be construed as personalized investment advice. There is no guarantee that the views and opinions expressed in this newsletter will come to pass. Investing in the stock and bond markets involves gains and losses and may not be suitable for all investors. Information presented herein is subject to change without notice. Horter has experienced periods of underperformance in the past and may also in the future. The returns represented herein are total return inclusive of reinvesting all interest and dividends.

The above equity, bond and cash weightings are targets and may not be the exact current weightings in any particular client account. Specifically, there may be cases where accounts hold higher cash levels than stated in these target weightings. This is usually to accommodate account level activity. Furthermore, some variable annuity and variable universal life accounts may not be able to purchase the exact weightings that we are indicating above due to specific product restrictions, limitations, riders, etc. Please refer to your client accounts for more specifics or call your Horter Investment Management, LLC at (513) 984-9933.

Investment advisory services offered through Horter Investment Management, LLC, a SEC-Registered Investment Advisor. Horter Investment Management does not provide legal or tax advice. Investment Advisor Representatives of Horter Investment Management may only conduct business with residents of the states and jurisdictions in which they are properly registered or exempt from registration requirements. Insurance and annuity products are sold separately through Horter Financial Strategies, LLC. Securities transactions for Horter Investment Management clients are placed through TCA by E*TRADE, TD Ameritrade and Nationwide Advisory Solutions.

For additional information about Horter Investment Management, LLC, including fees and services, send for our disclosure statement as set forth on Form ADV from Horter Investment Management, LLC using the contact information herein. Please read the disclosure statement carefully before you invest or send money.

Dow Jones – Week Ending

WEEKLY MARKET SUMMARY

Global Equities: US equity markets traded mixed within a narrow range despite an extremely important week for the world economy that included meetings between President Trump and North Korea’s Kim Jong Un, and monetary policy decisions by the US Federal Reserve (Fed, FOMC), the European Central Bank (ECB), and the Bank of Japan (BOJ). Friday announcements of tariffs on China caused selling of Dow Jones Industrial components which left the index down around 1% for the week. The S&P 500 ended slightly in the red, down around .02%, while the Nasdaq Composite gained nearly 1.4%. The Consumer Discretionary sector, led by Amazon (AMZN), helped the Nasdaq outperform and led all sectors for the week, with the Consumer Discretionary SPDR Select Sector ETF (XLY) gaining 1.9%. A Friday rout caused the Energy sector and its SPDR Select Sector ETF (XLE) to lose over 3.5%. A spike in the US dollar caused Emerging Market equities to slump, with the iShares MSCI Emerging Markets Index ETF (EEM) losing around 2.4% for the week. International Developed Markets and the iShares MSCI EAFE Index Fund ETF (EFA) finished down .55%.

Fixed Income: The yield on the US 10-Year Treasury Note was relatively stable, near 2.95%, until briefly spiking after the Fed statement indicated a higher expected path in interest rates. The spike above 3% was extremely short-lived and rates slipped back down near 2.92% to close the week. The market seemed to echo the Fed’s confidence in the strength of the US economy as high-yield bond funds saw net inflows, while the iShares IBoxx High-yield Corporate Bond ETF (HYG) had another solid week increasing almost .6%. The high-yield spread over corresponding risk-free securities tightened during the week, near 3.35%.

Commodities: Like most asset classes, the price of oil was steady-to-rising for most of the week. On Friday, one week before OPEC and non-OPEC Russia are set to meet and adjust the self-imposed production limit, oil prices fell around 3%. International Brent Crude ended the week down around 4%, near $73.40 per barrel. The American benchmark West Texas Intermediate (WTI) fell to $64.97 per barrel, down only a little over 1%, for the week. Natural Gas prices rose during the week to the highest price since winter of this year, over $3.00/MMBtu.

WEEKLY ECONOMIC SUMMARY

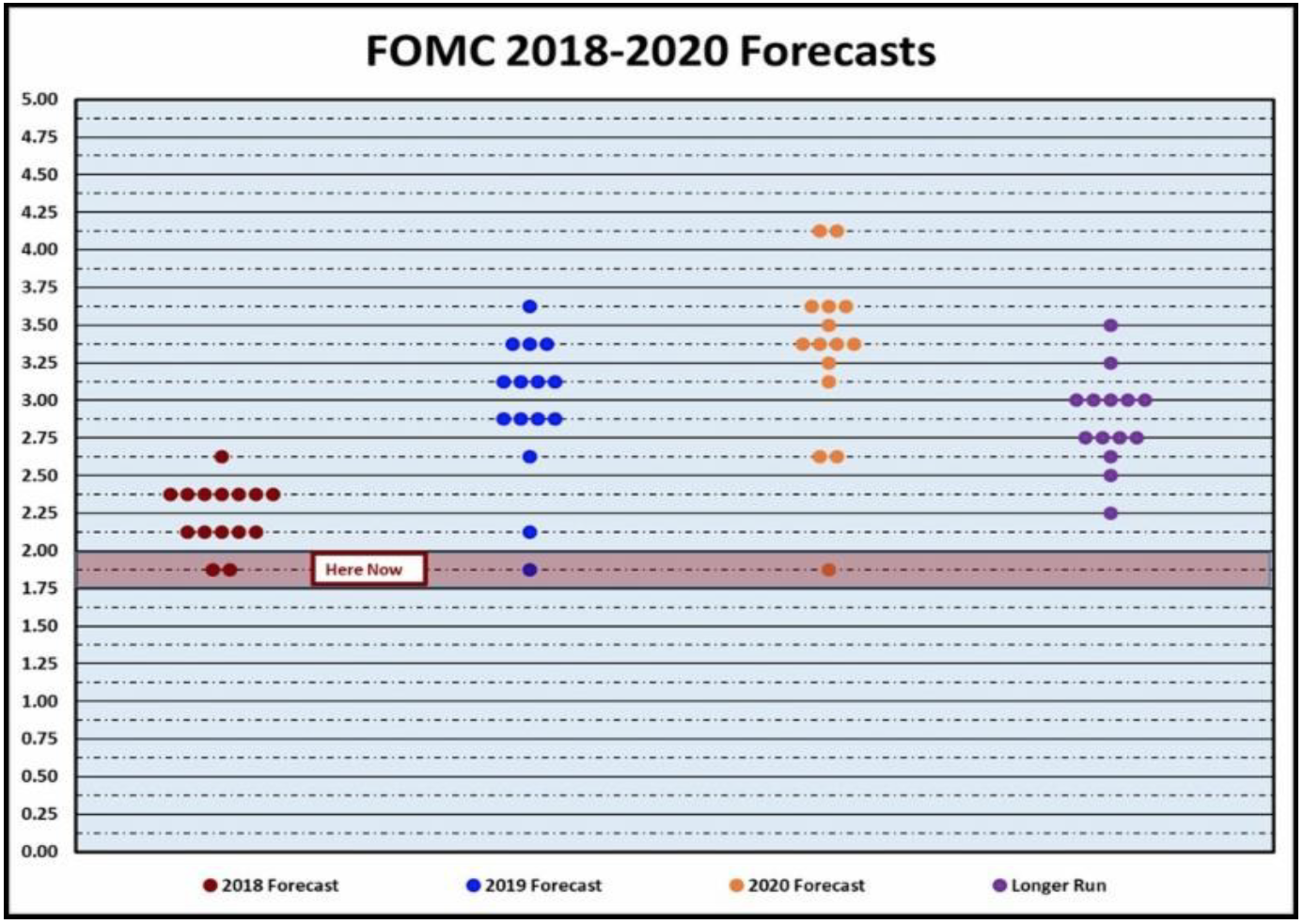

FOMC Announcement: The Federal Reserve Open Market Committee (FOMC) boosted its benchmark Federal Funds rate another .25% to a target range of 1.75-2.00% in a well communicated and widely anticipated move to help moderate inflationary pressure on the economy. With the rate hike during this June meeting a near certainty, market participants scrutinized the statement release and subsequent press conference with Chairman Jerome Powell for hints of changes to future monetary policy. The Chart of the Week (below) indicates the expected path of year-end Fed Funds rates, which were adjusted upward for 2018. Chairman Powell also indicated that the FOMC will start to have press conferences following every meeting starting in January 2019, in an effort to improve communication, while adding “Having twice as many press conferences does not signal anything about the timing or pace of future interest rate changes.”

ECB Announcement: The ECB announced that its €30 billion per month bond buying stimulus program will likely be tapered starting after September and concluded at the end of this year. ECB President Mario Draghi also indicated that it is unlikely to raise interest rates prior to the summer of 2019, and will be data dependent on maintaining its target level of inflation. German Bund yields and the Euro currency went lower on the news as the hawkish end of quantitative easing was cancelled out by the dovish policy surrounding interest rates.

Retail Sales: The latest retail sales data released by the US Census Bureau was much better than the .4% consensus estimate, with a .8% month-on-month (MoM) increase for the month of May. The report adjusts for seasonal variations; however, it does not account for higher prices paid. So, while the increase of consumption is welcome for boosting nominal GDP, inflation’s effect on the consumer is daunting as restaurants and clothing store sales indicated solid increases, but were dwarfed by gasoline station sales up 17.7% from the same period in 2017.

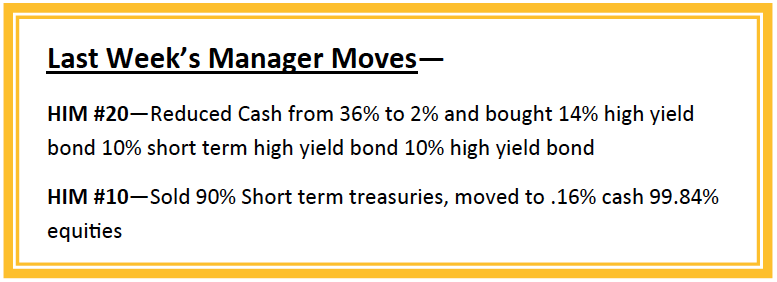

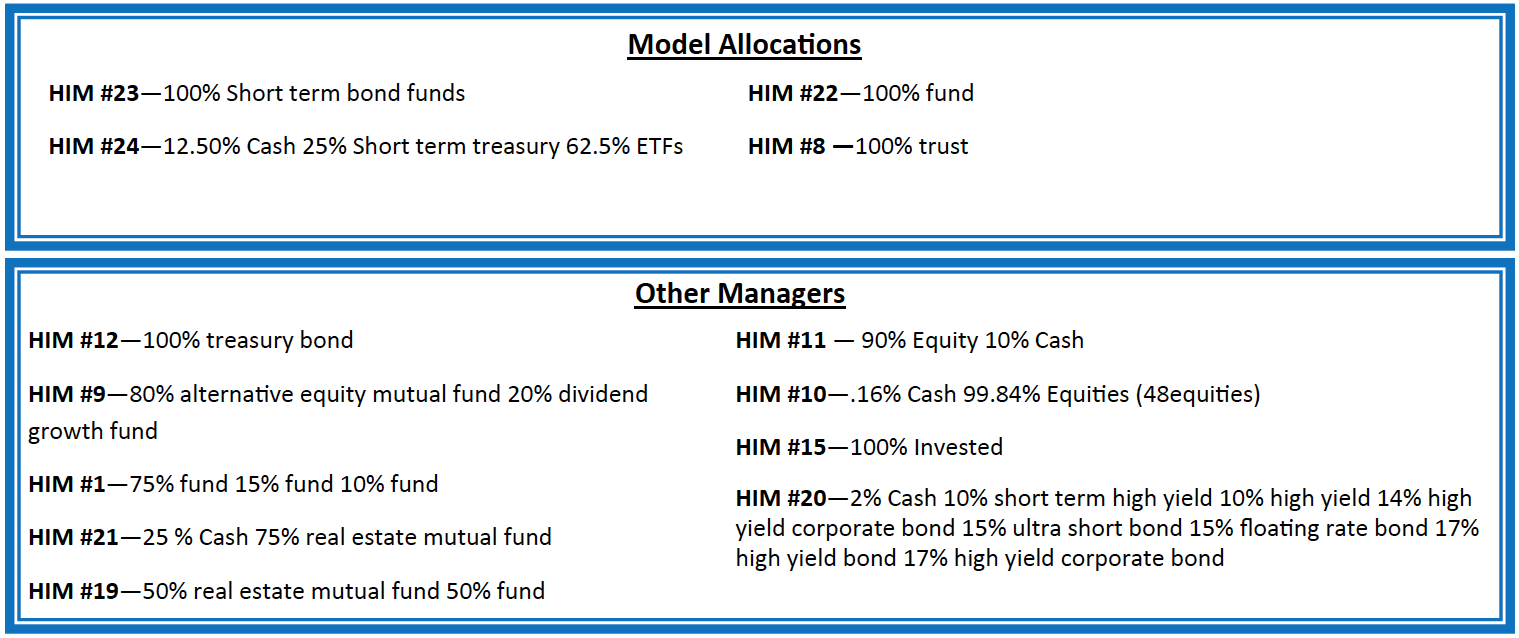

Current Model Allocations

Summary

In utilizing an approach that seeks to limit volatility, it is important to keep perspective of the activity in multiple asset classes. We seek to achieve superior risk-adjusted returns over a full market cycle to a traditional 60% equities / 40% bonds asset allocation. We do this by implementing global mandates of several tactical managers within different risk buckets. For those investors who are unwilling to stomach anything more than minimal downside risk, our goal is to provide a satisfying return over a full market cycle compared to the Barclays Aggregate Bond Index. At Horter Investment Management we realize how confusing the financial markets can be. It is important to keep our clients up to date on what it all means, especially with how it relates to our private wealth managers and their models. We are now in year nine of the most recent bull market, one of

the longest bull markets in U.S. history. At this late stage of the market cycle, it is extremely common for hedged managers to underperform, as they are seeking to limit risk. While none of us know when a market correction will come, even though the movement and volatility sure are starting to act like a correction, our managers have been hired based on our belief that they can accomplish a satisfying return over a full market cycle, — while limiting risk in comparison to a traditional asset allocation approach. At Horter we continue to monitor all of the markets and how our managers are actively managing their portfolios. We remind you there are opportunities to consider with all of our managers. Hopefully this recent market commentary is helpful and thanks for your continued trust and loyalty.