HORTER INVESTMENT MANAGEMENT, LLC

Weekly Commentary horterinvestment.com June 11, 2018

The Fed’s Fight for Control of Its Key Interest Rate: QuickTake

If a ship crossing a wide and placid harbor yaws so far that it al-most hits the channel markers, its captain might want to have its rudder adjusted. That’s what the Federal Reserve is considering as the fed funds rate threatens to slip outside the central bank’s tar-get range. The gap between the rate and the Fed’s upper bound has narrowed to a 7-1/2 year low, setting off alarm bells from Washington to Wall Street. It’s also prompted policy makers to discuss whether shifting tides in short-term markets mean they need to change the way they go about manipulating what is arguably the most important interest rate in the world. 1. What’s going on?

In December 2015, the Fed responded to improving economic conditions by raising interest rates that it had cut to near zero during the financial crisis. It set a target range for the fed funds rate of 0.25 percent to 0.5 percent. Since then it’s increased the range five times, to 1.50 percent to 1.75 percent currently, and is on the cusp of doing so again Wednesday. For most of that time, the effective fed funds rate – the average of what borrowers in the market actually paid – rested comfortably near the range’s mid-point, just like it’s supposed to. But since the beginning of the year, fed funds has been creeping higher, now sitting just five basis points below the top of the range at 1.70 percent. 2. What is the fed funds rate? It’s the rate at which big banks make overnight loans to each other from the reserves they keep on deposit at the Fed. Because it’s the basis for everything from credit card and auto loan rates to certificate of deposit yields, officials use a range of policy tools to exert control over it and thereby influence the direction of the broader economy.

Bernanke Says U.S. Economy Faces a ‘Wile E. Coyote’ Moment in 2020

U.S. economic growth could face a challenging slowdown as the Trump Administration’s powerful fiscal stimulus fades after two years, according to former Federal Reserve Chairman Ben Bernanke.

Bernanke said the $1.5 trillion in personal and corporate tax cuts and a $300 billion increase in federal spending signed by President Donald Trump “makes the Fed’s job more difficult all around” be-cause it’s coming at a time of very low U.S. unemployment.

“What you are getting is a stimulus at the very wrong moment,” Bernanke said Thursday during a policy discussion at the American Enterprise Institute, a Washington think tank. “The economy is already at full employment.”

The stimulus “is going to hit the economy in a big way this year and next year, and then in 2020 Wile E. Coyote is going to go off the cliff,” Bernanke said, referring to the hapless character in the Road Runner cartoon series. Sorry, Mr. President, But Best Economy Was Eisenhower’s (1)

The timing of Bernanke’s possible slowdown would line up badly for Trump, who has called the current economy the best ever and faces reelection in late-2020.

Bernanke, who stepped down from the U.S. central bank in 2014, is a distinguished fellow in residence at the Brookings Institution in Washington. Growth Slowdown

The Congressional Budget Office forecast in April that the stimulus would lift growth to 3.3 percent this year and 2.4 percent in 2019, compared with 2.6 percent in 2017. GDP growth slows to 1.8 percent in 2020 in the CBO projections. Fed officials predicted 2 percent growth in 2020 in their March median projection.

The degree of slowdown as stimulus fades is a matter of debate among economists, with some predicting the effects could last beyond two years if the U.S. boosts its capital stock and upgrades its workforce during this period of strong growth. Congress could also write new spending laws to smooth out the program, Bernanke noted.

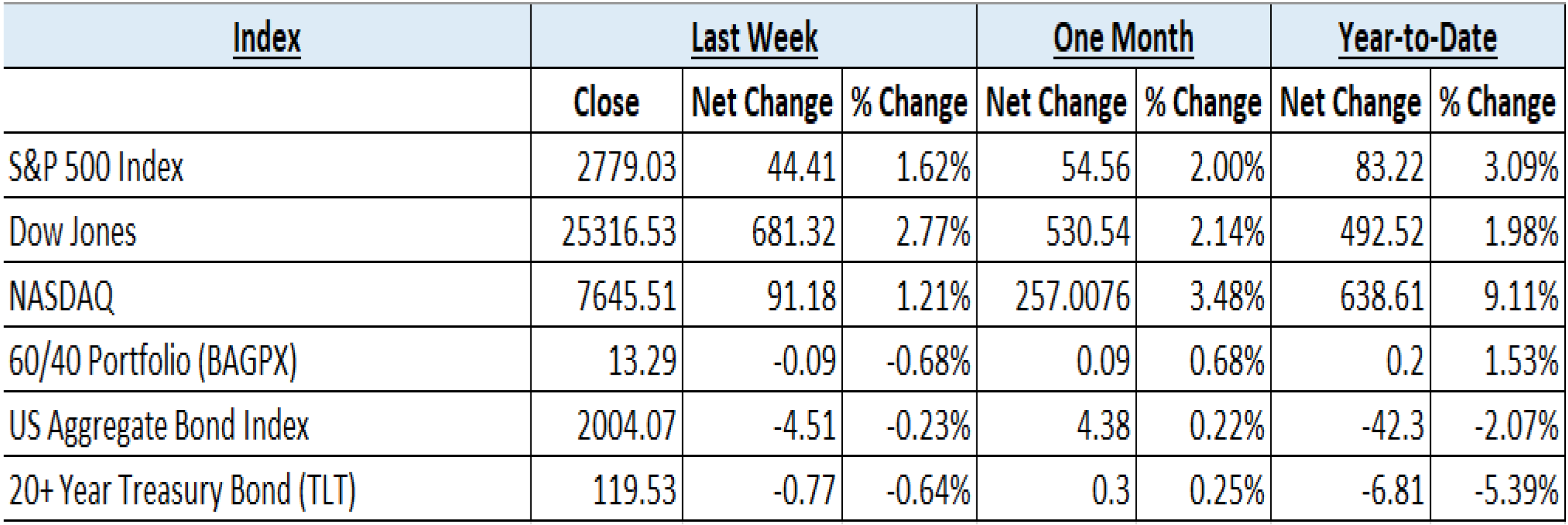

Taking a comprehensive look at the overall current stock market

Taking a comprehensive look at the overall current stock market, you can see the chart below representing eight major indices and their returns through the week ending June 11, 2018. In a truly diversified portfolio, the portfolio’s total return is determined by the performance of all of the individual positions in combination – not individually.

So, understanding the combined overall performance of the indices below, simply average the 3 indices to get a better overall picture of the market. The combined average of all 3 indices is -1.98% year to date.

Data Source: Investors FastTrack, Yahoo Finance

Past performance is not a guarantee of future results. This Update is limited to the dissemination of general information pertaining to its investment advisory services and is not suitable for everyone. The information contained herein should not be construed as personalized investment advice. There is no guarantee that the views and opinions expressed in this newsletter will come to pass. Investing in the stock and bond markets involves gains and losses and may not be suitable for all investors. Information presented herein is subject to change without notice. Horter has experienced periods of underperformance in the past and may also in the future. The returns represented herein are total return inclusive of reinvesting all interest and dividends.

The above equity, bond and cash weightings are targets and may not be the exact current weightings in any particular client account. Specifically, there may be cases where accounts hold higher cash levels than stated in these target weightings. This is usually to accommodate account level activity. Furthermore, some variable annuity and variable universal life accounts may not be able to purchase the exact weightings that we are indicating above due to specific product restrictions, limitations, riders, etc. Please refer to your client accounts for more specifics or call your Horter Investment Management, LLC at (513) 984-9933.

Investment advisory services offered through Horter Investment Management, LLC, a SEC-Registered Investment Advisor. Horter Investment Management does not provide legal or tax advice. Investment Advisor Representatives of Horter Investment Management may only conduct business with residents of the states and jurisdictions in which they are properly registered or exempt from registration requirements. Insurance and annuity products are sold separately through Horter Financial Strategies, LLC. Securities transactions for Horter Investment Management clients are placed through TCA by E*TRADE, TD Ameritrade and Nationwide Advisory Solutions.

For additional information about Horter Investment Management, LLC, including fees and services, send for our disclosure statement as set forth on Form ADV from Horter Investment Management, LLC using the contact information herein. Please read the disclosure statement carefully before you invest or send money.

Dow Jones – Week Ending

WEEKLY MARKET SUMMARY

Global Equities: All major US equity indices ended the week higher, but this time, without leadership from the Technology sector. With the high-flying “FANG” stocks relatively over-bought, the Dow Jones Industrial Average took leadership, gaining around 2.7% for the week. The S&P 500 gained over 1.5% for the week, while the Nasdaq Composite gained a respectable 1.1%. The Consumer Discretionary sector edged out the small Materials sector to lead all sectors for the week, with the Consumer Discretionary SPDR Select Sector ETF (XLY) gaining over 3%. The defensive Utilities sector and its SPDR Select Sector ETF (XLU) lost over 3%. Emerging Market equities had a tough week thanks to market turmoil in Brazil, yet the iShares MSCI Emerging Markets Index ETF (EEM), with 5.5% exposure to the country, was virtually unchanged for the week. International Developed Markets and the iShares MSCI EAFE Index Fund ETF (EFA) ended with nearly a .6% increase.

Fixed Income: The yield on the US 10-Year Treasury Note rose during the week, briefly touching the 3% level before pulling back on Thursday thanks to a rout in the Brazilian currency and equity market. The flight to safety is part of the latest bout of Emerging Market weakness, this time, stemming from Brazil’s slow growth and labor market unrest. High-yield (HY) spreads over corresponding risk-free securities tightened during the week near 3.45%, as the iShares IBoxx High-yield Corporate Bond ETF (HYG) increased almost .6%.

Commodities: Oil prices dipped around 2% in the beginning of the week due, in part, by a Bloomberg report that the Trump administration had quietly requested Saudi Arabia to increase OPEC oil production output to help curb price increases stemming from US sanctions on Iran. Opinions vary dramatically over the direction of the next price move, and looks to be in a holding pattern until the next meeting amongst OPEC members, on June 22. Both Brent Crude and American West Texas Intermediate (WTI), ended the week virtually unchanged from the prior week near $76.75 and $65.77 per barrel, respectively. Natural Gas prices spiked after a bullish EIA inventory report, but ended the week down over 2.5% near $2.89/MMBtu.

WEEKLY ECONOMIC SUMMARY

Employment Situation: The US Census Bureau announced a $1 billion reduction in the US goods and services trade deficit for the month of April versus the revised March level. The deficit dropped 2.1% to $46.2 billion thanks to a decline in imports and a record high level of exports of $211.2 billion. The export of goods increased mainly due to oil, other petroleum products, corn, and soybeans, helping to off-set a $2.8 billion decrease in exports of civilian aircraft. Service exports including financial services, charges for use of intellectual property, and other business services grew equally on an absolute basis, but relatively higher than the export of goods thanks to being only 1/3 of total exports.

US Weekly Jobless Claims: New jobless claims unexpectedly fell for the measurement period to 222,000 from the prior revised figure of 223,000 on a seasonally adjusted basis. The result is much better than the consensus estimate of 225,000, and signals continued strength and an even tighter labor market. The 4-week moving average of continuing claims fell to 1.73 million, the lowest level since 1973, setting the stage for the expected .25% federal funds rate hike announcement after the Federal Reserve Open Market Committee meeting, next week.

Consumer Credit: The consumer credit report released Federal Reserve indicated a seasonally adjusted 2.9% annualized increase in total consumer credit outstanding for the month of April. Revolving credit, or credit card debt, increased 2.6% after a March decline and small increases during January and February. It may be that many Americans have used the extra cash from the tax cuts to pay down previously outstanding debt during the 1st quarter of 2018, a good sign for a consumer spending rebound for 2nd quarter GDP.

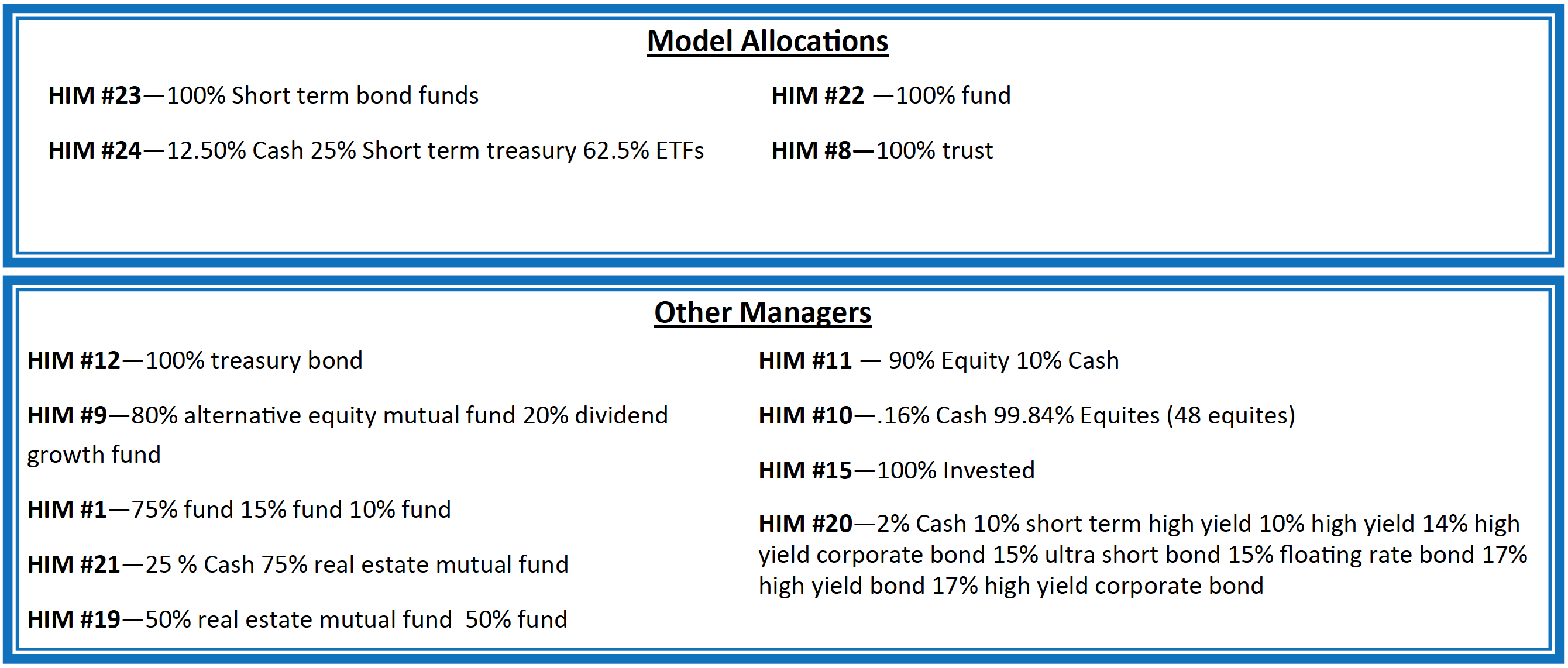

Current Model Allocations

Summary

In utilizing an approach that seeks to limit volatility, it is important to keep perspective of the activity in multiple asset classes. We seek to achieve superior risk-adjusted returns over a full market cycle to a traditional 60% equities / 40% bonds asset allocation. We do this by implementing global mandates of several tactical managers within different risk buckets. For those investors who are unwilling to stomach anything more than minimal downside risk, our goal is to provide a satisfying return over a full market cycle compared to the Barclays Aggregate Bond Index. At Horter Investment Management we realize how confusing the financial markets can be. It is important to keep our clients up to date on what it all means, especially with how it relates to our private wealth managers and their models. We are now in year nine of the most recent bull market, one of

the longest bull markets in U.S. history. At this late stage of the market cycle, it is extremely common for hedged managers to underperform, as they are seeking to limit risk. While none of us know when a market correction will come, even though the movement and volatility sure are starting to act like a correction, our managers have been hired based on our belief that they can accomplish a satisfying return over a full market cycle, —while limiting risk in comparison to a traditional asset allocation approach. At Horter we continue to monitor all of the markets and how our managers are actively managing their portfolios. We remind you there are opportunities to consider with all of our managers. Hopefully this recent market commentary is helpful and thanks for your continued trust and loyalty.