HORTER INVESTMENT MANAGEMENT, LLC

Weekly Commentary horterinvestment.com February 4, 2019

Bond King Jeffrey Gundlach says we just got ‘the most recessionary signal’ yet

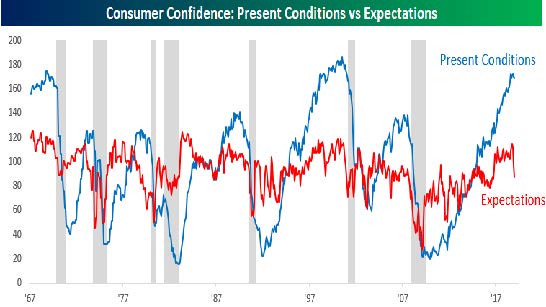

Drooping consumer sentiment is pointing the way to a substantial economic slowdown, if history is any guide.

In particular, the gap between current sentiment and future expectations has blown out wider, according to the Conference Board’s Consumer Confidence Index released Tuesday.

While confidence in the broader confidence index remains strong, falling just slightly month over month, the Expectations Index tumbled from 97.7 to 87.3 from December. Since October, the expectations reading has plunged 24 percent. Conversely, the Present Situation Index is at 169.6, a nudge lower from December’s reading.

Such wide gaps have portended sharp declines in economic activity, as pointed out by several market observers, including DoubleLine Capital’s Jeffrey Gundlach, the so-called Bond King.

“The most recessionary signal at present is consumer future expectations relative to current conditions. It’s one of the worst readings ever,” he said in a tweet.

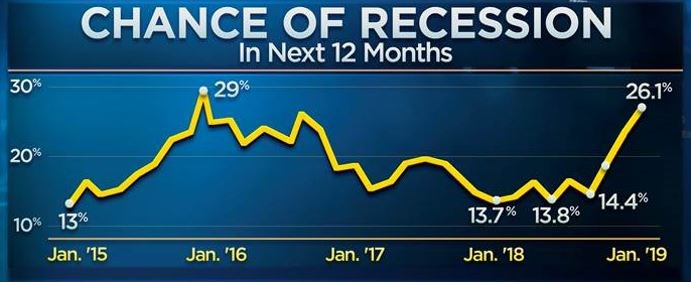

Odds of a recession spike to a three-year high, according to CNBC’s Fed survey

The chance of recession in the next 12 months spiked to its highest level in three years as market participants ratcheted up their worries about global economic weakness, Fed rate hikes, the market sell-off, trade tensions and the government shutdown.

The CNBC Fed Survey, conducted last week while the government was still shut down, saw the probability of a recession in the next 12 months rise to 26 percent, the third straight increase. The probability was last higher at nearly 29 percent in January 2016, following another market sell-off, showing how sensitive the outlook for survey respondents can be to market gyrations.

“When you look at the slide in global growth, it is hard to think that, in a matter of time, the U.S. won’t join the slide,” Kevin Giddis, head of fixed income capital markets at Raymond James Financial, wrote in response to the survey. “This prospect has only been enhanced by a lack of a trade deal, the government shutdown, and a completely inefficient cooperation in Washington.”

Taking a comprehensive look at the overall current stock market

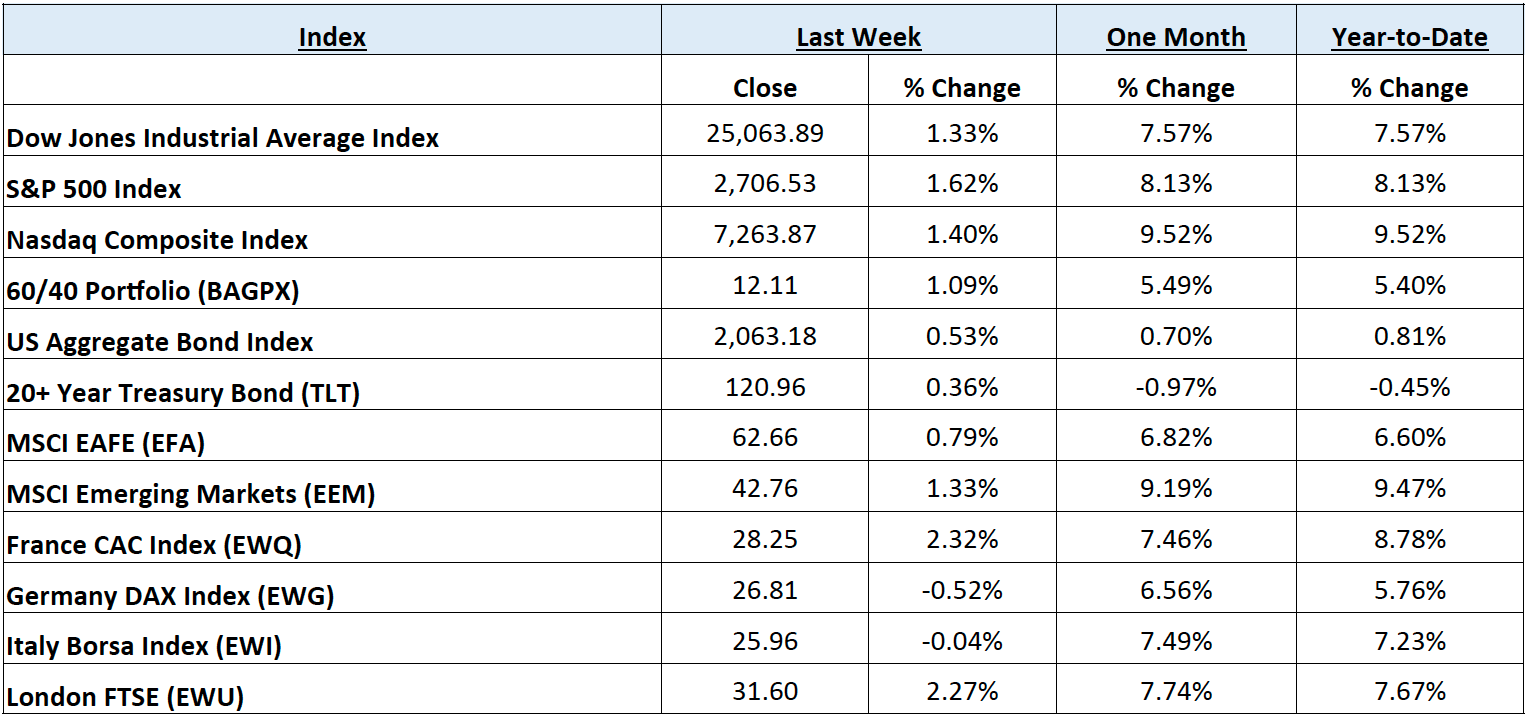

Taking a comprehensive look at the overall current stock market, you can see the chart below representing eight major indices and their returns through the week ending February 1, 2019. In a truly diversified portfolio, the portfolio’s total return is determined by the performance of all of the individual positions in combination – not individually.

So, understanding the combined overall performance of the indices below, simply average the 12 indices to get a better overall picture of the market. The combined average of all 12 indices is 6.37% year to date.

Data Source: Investors FastTrack, Yahoo Finance, Investopedia

Past performance is not a guarantee of future results. This Update is limited to the dissemination of general information pertaining to its investment advisory services and is not suitable for everyone. The information contained herein should not be construed as personalized investment advice. There is no guarantee that the views and opinions expressed in this newsletter will come to pass. Investing in the stock and bond markets involves gains and losses and may not be suitable for all investors. Information presented herein is subject to change without notice. Horter has experienced periods of underperformance in the past and may also in the future. The returns represented herein are total return inclusive of reinvesting all interest and dividends.

The above equity, bond and cash weightings are targets and may not be the exact current weightings in any particular client account. Specifically, there may be cases where accounts hold higher cash levels than stated in these target weightings. This is usually to accommodate account level activity. Furthermore, some variable annuity and variable universal life accounts may not be able to purchase the exact weightings that we are indicating above due to specific product restrictions, limitations, riders, etc. Please refer to your client accounts for more specifics or call your Horter Investment Management, LLC at (513) 984-9933.

Investment advisory services offered through Horter Investment Management, LLC, a SEC-Registered Investment Advisor. Horter Investment Management does not provide legal or tax advice. Investment Advisor Representatives of Horter Investment Management may only conduct business with residents of the states and jurisdictions in which they are properly registered or exempt from registration requirements. Insurance and annuity products are sold separately through Horter Financial Strategies, LLC. Securities transactions for Horter Investment Management clients are placed through E*TRADE Advisor Services, TD Ameritrade and Nationwide Advisory Solutions.

For additional information about Horter Investment Management, LLC, including fees and services, send for our disclosure statement as set forth on Form ADV from Horter Investment Management, LLC using the contact information herein. Please read the disclosure statement carefully before you invest or send money.

Dow Jones – Week Ending

WEEKLY MARKET SUMMARY

Global Equities: The US Federal Reserve (FOMC/Fed) has seemingly confirmed with its Wednesday announcement what markets have been expecting since the beginning of the year, an end to the current tightening cycle. This allowed US equity markets to rise above technical levels of resistance, with the S&P 500 Index, the Dow Jones Industrial Average, and the Nasdaq Composite Index reversing early week slumps to return 1.57%, 1.32%, and 1.38% respectively. The Energy sector made a Friday surge to edge out Communications Services to lead all S&P 500 sectors for the week, as the Energy Select Sector SPDR ETF (XLE) gained 1.74%. The Fed announcement was even better news for Emerging Market equities who rely heavily on US investment to fund relatively high rates of growth. This was evident in continued outperformance of the iShares MSCI Emerging Market Index ETF (EEM) gaining 2.39% on the week.

Fixed Income: The important Fed announcement was also a boon for bonds, as the 10-year US Treasury Note yield back to 2.68% from above 2.75% at the close of the previous week. This move that resembled a flight to safety was anything but, as investors piled back into credit with high yield spreads continuing to drop despite an increase in issuance of $9.45B during the week, according to Bloomberg. Lipper reported slight inflows into high yield bond funds, as the iShares IBoxx High Yield Corporate Bond ETF (HYG) returned .78% on a total return basis for the week.

Commodities: Commodities received a boost from the Fed, as well, as oil prices climbed after the prior week’s pull-back to post gains of roughly 18%, for the best January on record. The evolving political situation in Venezuela and European companies looking to continue business with Iran may help to slow the grind higher for oil prices in the near term. The West Texas Intermediate (WTI) benchmark gained 2.92%, while the International Brent crude benchmark gained 1.8% during the week, to close near $55.26 and $62.75 per barrel, respectively. Natural gas prices were slammed another -14% despite the polar vortex affecting much of the country, to close the week at $2.73/MMBtu.

WEEKLY ECONOMIC SUMMARY

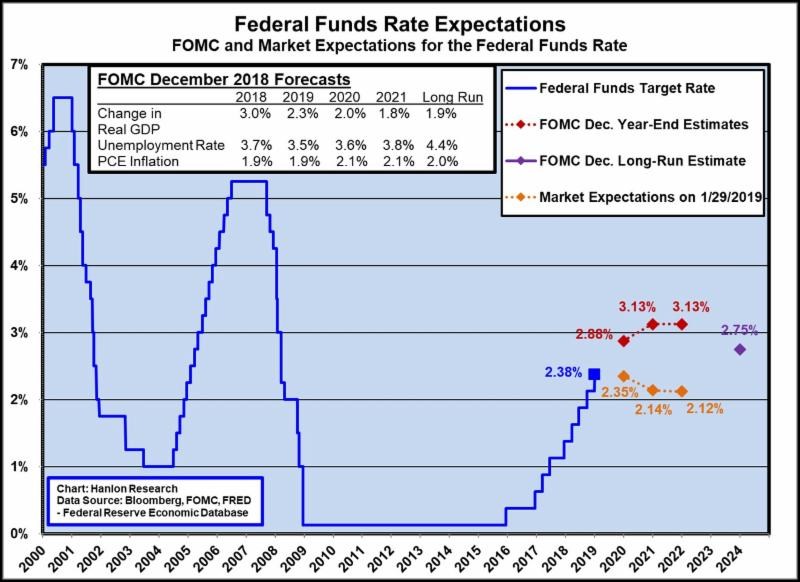

FOMC Announcement: The Federal Open Market Committee left its benchmark Federal Funds rate unchanged, as anticipated, after the most recent meeting on Wednesday. The pause is consistent with what the Fed had communicated at the prior meeting, and with what individual members have been saying publicly since, emphasizing patience in light of global economic developments and muted inflation pressure. The Fed did surprise with even more dovish news that it is prepared to adjust the balance sheet normalization earlier than previously stated, which is currently targeted at $50B per month. Market odds now favor an interest rate cut rather than a hike for the rest of 2019.

Employment Situation: The Employment Situation report by the Bureau of Labor Statistics indicated another strong increase in Nonfarm Payrolls for the month of January. The surprising increase of 304,000 versus the consensus estimate of 158,000 made up for a lower revision of the number for December. Construction, trade, and transportation jobs highlight the sectors adding jobs for the month. The unemployment rate ticked higher to 4% thanks, again, to an increase in the participation rate. The report also signaled moderation in wage pressure, missing the consensus estimate of .3%, rising only .1% for the month. The average work week was unchanged and inline with consensus at 34.5 hours.

Q4 Earnings Season: Amazon (AMZN), Apple Inc. (AAPL), and Facebook (FB) highlighted an extremely busy Q4 earnings week. FB stock gained over 10% thanks to a blowout quarter, surprising analysts as advertisers and new users continue to flock to the platform despite privacy concerns. AAPL shares were steady despite disappointing revenue and unit sales of its flagship iPhone, as customers hold onto their older models for longer. AAPL says that this is ok because consumers are sticking within the ecosystem and spending more on subscription services. AMZN somehow failed to impress with record-breaking sales and earnings which included explosive growth for its Amazon Web Services segment, ending the week down 2.65%. With 57.7% of S&P 500 companies having reported 4th quarter earnings, the 2019 forward P/E (on reported earnings) is 17.53.

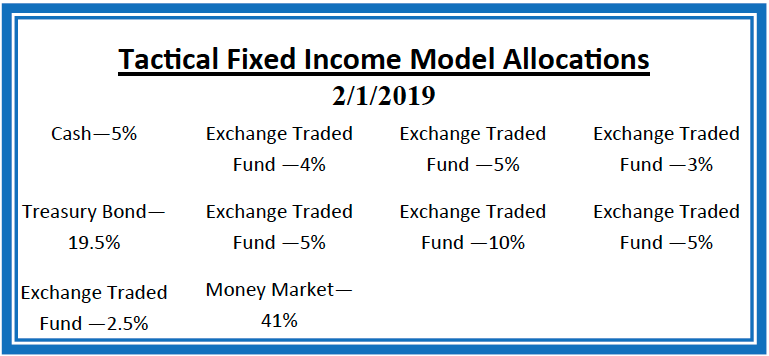

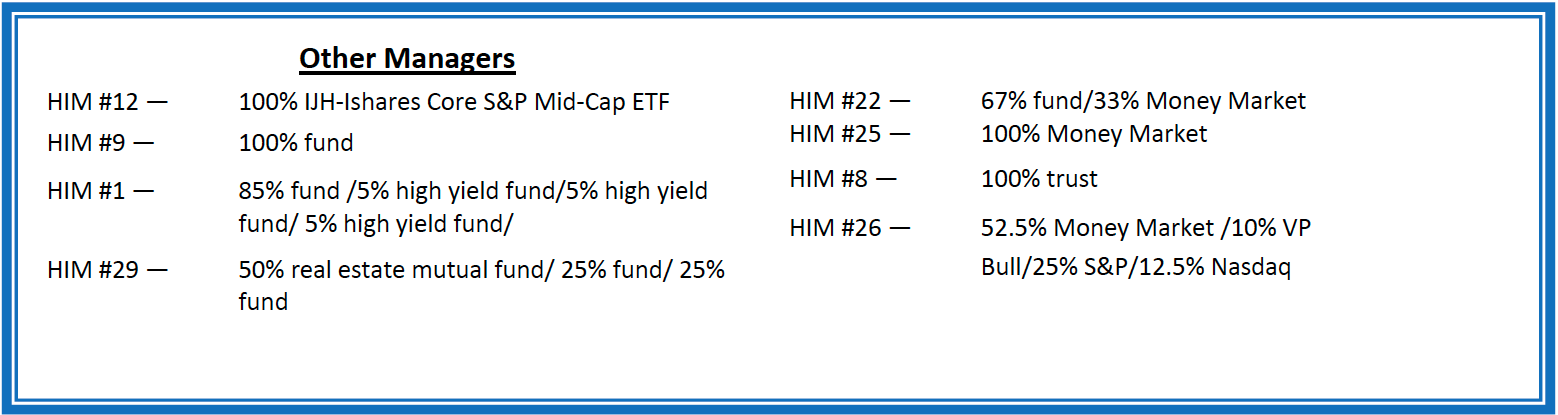

Current Model Allocations

Summary

In utilizing an approach that seeks to limit volatility, it is important to keep perspective of the activity in multiple asset classes. We seek to achieve superior risk-adjusted returns over a full market cycle to a traditional 60% equities / 40% bonds asset allocation. We do this by implementing global mandates of several tactical managers within different risk buckets. For those investors who are unwilling to stomach anything more than minimal downside risk, our goal is to provide a satisfying return over a full market cycle compared to the Barclays Aggregate Bond Index. At Horter Investment Management we realize how confusing the financial markets can be. It is important to keep our clients up to date on what it all means, especially with how it relates to our private wealth managers and their models. We are now in year nine of the most recent bull market, one of

the longest bull markets in U.S. history. At this late stage of the market cycle, it is extremely common for hedged managers to underperform, as they are seeking to limit risk. While none of us know when a market correction will come, even though the movement and volatility sure are starting to act like a correction, our managers have been hired based on our belief that they can accomplish a satisfying return over a full market cycle, – while limiting risk in comparison to a traditional asset allocation approach. At Horter we continue to monitor all of the markets and how our managers are actively managing their portfolios. We remind you there are opportunities to consider with all of our managers. Hopefully this recent market commentary is helpful and thanks for your continued trust and loyalty.