HORTER INVESTMENT MANAGEMENT, LLC

Weekly Commentary horterinvestment.com February 25, 2019

Treasury yields fall amid US-China trade talks

U.S. government debt yields fell on Friday as trade talks between the U.S. and China continued.

The yield on the benchmark 10-year Treasury note fell to around 2.648 percent, while the yield on the 30-year Treasury bond dipped to 3.007 percent. Bond yields move inversely to prices.

Market players continue to monitor the latest round of negotiations between Washington and Beijing. Optimism has risen over the chances of both countries securing a deal to end their protracted trade war, but some experts say the most difficult part is yet to come as high level talks continue into Friday.

“There’s obviously an incentive for both sides to reach a deal,” James Athey, senior investment manager at Aberdeen Standard Investments, told CNBC’s “Squawk Box Europe” on Friday.

“The problem is that you’re now getting to the more difficult part of the negotiation, which is things like the IP (intellectual property) problem.”

After climbing to start 2019, the stock market comeback is on hold – here’s why

The Dow Jones Industrial Average clinched its first three day loss of 2019 on Friday and there are a few key reasons the stock market’s recent rally has slowed.

The Dow and S&P 500 indexes each climbed over 7 percent in the past six weeks, but the rally in U.S. stocks has paused. The Dow was headed for its first negative week of the year but narrowly eked out an 0.17 percent gain after a late rally on Friday afternoon.

But according to National Securities’ Art Hogan the win streak could go badly at anytime.

“We’re probably going to have a bit of a consolidation period in front of us,” he said Wednesday on CNBC’s “Trading Na-tion” — pointing to the sheer magnitude of gains in a short time span.

When the Dow’s 10-week win streak ended on May 12, 1995, it fell 2 percent the following week. Ultimately, the blue chip index was flat over the next month.

This time around, Hogan predicts a more volatile outcome.

“If you look back to the December low and the 18 percent pop we’ve had since then, … it makes sense to have a week or two of consolidation,” he said.

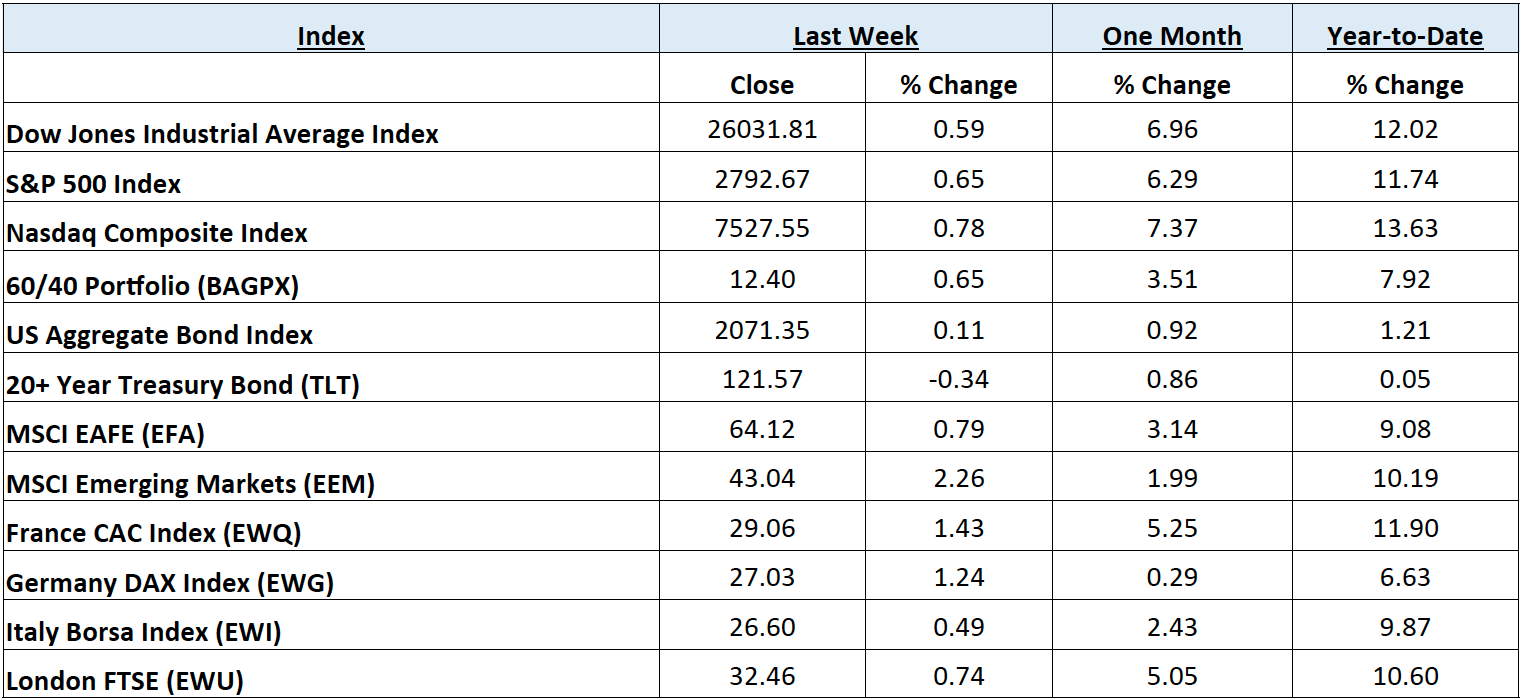

Taking a comprehensive look at the overall current stock market

Taking a comprehensive look at the overall current stock market, you can see the chart below representing eight major indices and their returns through the week ending February 22, 2019. In a truly diversified portfolio, the portfolio’s total return is determined by the performance of all of the individual positions in combination – not individually.

So, understanding the combined overall performance of the indices below, simply average the 12 indices to get a better overall picture of the market. The combined average of all 12 indices is 8.74% year to date.

Data Source: Investors FastTrack, Yahoo Finance, Investopedia

Past performance is not a guarantee of future results. This Update is limited to the dissemination of general information pertaining to its investment advisory services and is not suitable for everyone. The information contained herein should not be construed as personalized investment advice. There is no guarantee that the views and opinions expressed in this newsletter will come to pass. Investing in the stock and bond markets involves gains and losses and may not be suitable for all investors. Information presented herein is subject to change without notice. Horter has experienced periods of underperformance in the past and may also in the future. The returns represented herein are total return inclusive of reinvesting all interest and dividends.

The above equity, bond and cash weightings are targets and may not be the exact current weightings in any particular client account. Specifically, there may be cases where accounts hold higher cash levels than stated in these target weightings. This is usually to accommodate account level activity. Furthermore, some variable annuity and variable universal life accounts may not be able to purchase the exact weightings that we are indicating above due to specific product restrictions, limitations, riders, etc. Please refer to your client accounts for more specifics or call your Horter Investment Management, LLC at (513) 984-9933.

Investment advisory services offered through Horter Investment Management, LLC, a SEC-Registered Investment Advisor. Horter Investment Management does not provide legal or tax advice. Investment Advisor Representatives of Horter Investment Management may only conduct business with residents of the states and jurisdictions in which they are properly registered or exempt from registration requirements. Insurance and annuity products are sold separately through Horter Financial Strategies, LLC. Securities transactions for Horter Investment Management clients are placed through E*TRADE Advisor Services, TD Ameritrade and Nationwide Advisory Solutions.

For additional information about Horter Investment Management, LLC, including fees and services, send for our disclosure statement as set forth on Form ADV from Horter Investment Management, LLC using the contact information herein. Please read the disclosure statement carefully before you invest or send money.

Dow Jones – Week Ending

WEEKLY MARKET SUMMARY

Global Equities: While not necessarily close to a deal, the release of an outline for a potential US-China trade agreement helped US equities grind slightly higher as the major indices wedge between technical moving average support and resistance at prior highs. The S&P 500, the Dow Jones Industrial Average, and the Nasdaq Composite indices traded within a fairly narrow range with weekly gains of around .33%. International stocks performed better, with Developed International stocks represented by the iShares MSCI EAFE Index Fund ETF (EFA) gaining nearly .75%, while Emerging Market stocks resumed 2019 outperformance with the iShares MSCI Emerging Market Index ETF (EEM) up around 2% for the week.

Fixed Income: The yield on the 10-year US Treasury Note finished the week a basis point lower, at 2.65%, after kissing 2.7% late in the holiday-shortened trading week. The yield spread of the 10-year over the 2-year Treasury (10-2 spread) has stopped narrowing, although remaining fairly tight and trading sideways, since the dovish pivot from the Federal Reserve. This past week was no different, as the 10-2 spread remained near .15-.16% and does not look at risk of inversion. High yield bond spreads narrowed slightly, dropping below 4%, as the iShares IBoxx High Yield Corporate Bond ETF (HYG) gained nearly .2%. Lipper reported more net inflows into high yield funds of $284 million for the week ended 2/20.

Commodities: Continued commitment to OPEC+ production cuts have combined with rising US-China trade deal optimism for another week of gains for crude oil prices. This is despite record US production reported by the Energy Information Administration (EIA) for the week ended February 15th. The West Texas Intermediate (WTI) benchmark gained another 2.9% to $57.22 per barrel, while the International Brent crude benchmark gained over 1% to close near $67 per barrel. Natural gas prices rose slightly to $2.70/MMBtu.

WEEKLY ECONOMIC SUMMARY

FOMC Minutes: Wednesday’s release of the minutes from the January Federal Open Market Committee (FOMC/Fed) meeting provided more insight on the important shift from fairly aggressive tightening to a more neutral policy that included a likely sun-setting of the balance sheet runoff. This is despite the Fed’s own positive assessment of the US economy, citing a tight labor market, solid GDP, and strong household spending. Subdued inflation pressure has allowed the Fed this opportunity to be patient and monitor concerns in the US housing market, slowing foreign economies, and financial market warning signs that had been flashing brighter with each additional interest rate hike.

PMI Composite FLASH: The early estimate for the Purchasing Managers’ Index Composite is signaling weakness in manufacturing for the month of February. Strength in the higher-weighted services sector masked weakness in the headline composite number of 55.8 versus a consensus estimate of 54.4. Manufacturing sector respondents are reporting slowing production due to softness in client demand contributed to global slowing. Manufacturers, however, are still hiring at a solid pace, signaling that they may expect the softness to be transitory.

Q4 Earnings Season: The retail behemoth, Walmart (WMT), reported surging e-commerce sales that helped it to beat 4th quarter estimates for sales and earnings. The report flies in the face of the weak December retail sales report from the prior week, and perhaps raises the possibility of the reported “glitch” in that report versus WMT being a one-off retail brightspot. WMT stock roared 4% higher but had given back all the gains by the end of the week. Kraft Heinz Inc. (KHC) released a dismal report which missed expectations, lowered its dividend, disclosed a Securities Exchange Commission (SEC) investigation, and included a $15B write-down of its Oscar Meyer and Kraft brands. KHC stock, a major holding of Warren Buffett’s Berkshire Hathaway (BRK/A,BRK/B), took a dive, dropping at one point over -28% on Friday.

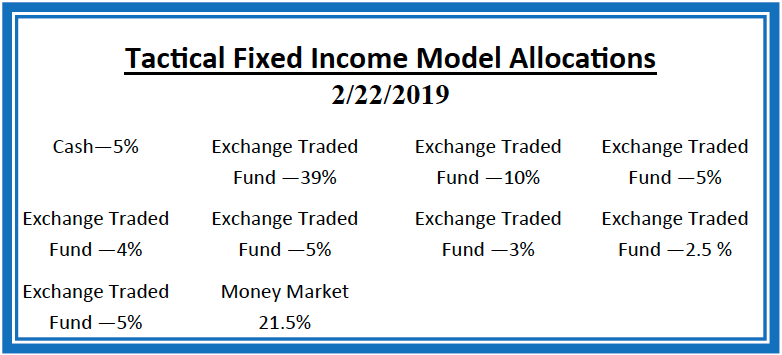

Current Model Allocations

Data Source: Hanlon Investment Management

Summary

In utilizing an approach that seeks to limit volatility, it is important to keep perspective of the activity in multiple asset classes. We seek to achieve superior risk-adjusted returns over a full market cycle to a traditional 60% equities / 40% bonds asset allocation. We do this by implementing global mandates of several tactical managers within different risk buckets. For those investors who are unwilling to stomach anything more than minimal downside risk, our goal is to provide a satisfying return over a full market cycle compared to the Barclays Aggregate Bond Index. At Horter Investment Management we realize how confusing the financial markets can be. It is important to keep our clients up to date on what it all means, especially with how it relates to our private wealth managers and their models. We are now in year nine of the most recent bull market, one of

the longest bull markets in U.S. history. At this late stage of the market cycle, it is extremely common for hedged managers to underperform, as they are seeking to limit risk. While none of us know when a market correction will come, even though the movement and volatility sure are starting to act like a correction, our managers have been hired based on our belief that they can accomplish a satisfying return over a full market cycle, – while limiting risk in comparison to a traditional asset allocation approach. At Horter we continue to monitor all of the markets and how our managers are actively managing their portfolios. We remind you there are opportunities to consider with all of our managers. Hopefully this recent market commentary is helpful and thanks for your continued trust and loyalty.

Data Source: Hanlon Investment Management