HORTER INVESTMENT MANAGEMENT, LLC

Weekly Commentary horterinvestment.com April 30, 2018

U.S. Pension Fund Collapse Isn’t a Distant Prospect. It Could Come in 5 Years.

Warnings about looming public pension disasters have regularly cropped up since the 1950s, pointing to problems 25 years or more down the line. To politicians and union leaders, the troubles were someone else’s predicament. Then crisis fatigue set in as the big problem remained down the road.

Today, the hard stop is five to 10 years away, within the career plans of current officials. In the next decade, and probably within five years, some large states are going to face insolvency due to pensions, absent major changes.

There are some reassuring facts. Many states are in pretty good shape, and many others still have time and resources to fix things. There is no serious chance of retirees being impoverished. What’s in doubt is whether states will pay promised benefits to retirees with large pensions or significant outside income or assets. Also, although most of the problem is created by politicians and union leaders cutting deals to promise future unfunded benefits to keep voters happy, there are also plenty of stories of politicians and union leaders risking their careers to stand up for honest pensions.

It’s important to distinguish between actuarial problems (the present value of projected future benefit payments exceeds the funds set aside to pay them plus projected future contributions) and cash problems (not having the money to send out this month’s checks). Actuarial problems are always debatable and usually involve the distant future. Cash shortfalls are undeniable and immediate.

New Jersey has $78 billion in its state pension fund, which is supposed to cover future payments with a present value of $280 billion. But that latter number is a projection. You can ignore it if you wish, or hope that soaring investment returns or a pandemic among retired workers will fix it. A more certain figure is that the $78 billion represents less than seven years of required cash payments.

U.S. March Consumer Spending Picks Up; Inflation Hits Fed Goal

U.S. consumer spending picked up in March while the Federal Reserve’s preferred inflation gauge hit the central bank’s 2 percent target for the first time in a year, reinforcing the outlook for further interest-rate hikes.

Purchases rose 0.4 percent from the prior month, matching estimates, after being little changed in February, Commerce Department figures showed Monday. The price gauge linked to consumption rose 2 percent from a year earlier after 1.7 percent in February; excluding food and energy, which officials see as a better gauge of underlying trends, it was up 1.9 percent.

Taking a comprehensive look at the overall current stock market

Taking a comprehensive look at the overall current stock market, you can see the chart below representing eight major indices and their returns through the week ending April 27, 2018. In a truly diversified portfolio, the portfolio’s total return is determined by the performance of all of the individual positions in combination – not individually.

So, understanding the combined overall performance of the indices below, simply average the 7 indices to get a better overall picture of the market. The combined average of all 7 indices is –1.09% year to date.

Data Source: Investors FastTrack, Yahoo Finance

Past performance is not a guarantee of future results. This Update is limited to the dissemination of general information pertaining to its investment advisory services and is not suitable for everyone. The information contained herein should not be construed as personalized investment advice. There is no guarantee that the views and opinions expressed in this newsletter will come to pass. Investing in the stock and bond markets involves gains and losses and may not be suitable for all investors. Information presented herein is subject to change without notice. Horter has experienced periods of underperformance in the past and may also in the future. The returns represented herein are total return inclusive of reinvesting all interest and dividends.

The above equity, bond and cash weightings are targets and may not be the exact current weightings in any particular client account. Specifically, there may be cases where accounts hold higher cash levels than stated in these target weightings. This is usually to accommodate account level activity. Furthermore, some variable annuity and variable universal life accounts may not be able to purchase the exact weightings that we are indicating above due to specific product restrictions, limitations, riders, etc. Please refer to your client accounts for more specifics or call your Horter Investment Management, LLC at (513) 984-9933.

Investment advisory services offered through Horter Investment Management, LLC, a SEC-Registered Investment Advisor. Horter Investment Management does not provide legal or tax advice. Investment Advisor Representatives of Horter Investment Management may only conduct business with residents of the states and jurisdictions in which they are properly registered or exempt from registration requirements. Insurance and annuity products are sold separately through Horter Financial Strategies, LLC. Securities transactions for Horter Investment Management clients are placed through TCA by E*TRADE, TD Ameritrade and Nationwide Advisory Solutions.

For additional information about Horter Investment Management, LLC, including fees and services, send for our disclosure statement as set forth on Form ADV from Horter Investment Management, LLC using the contact information herein. Please read the disclosure statement carefully before you invest or send money.

Dow Jones – Week Ending

WEEKLY MARKET SUMMARY

Global Equities: US equity performance was mixed, with the S&P 500 large cap index relatively unchanged, while the Nasdaq Composite and the Dow Jones Industrial Indexes were down around .5%. After a mid-week slump due to interest rates spiking above a key psychological level, equities bounced back with help from the European Central Bank (ECB) remaining accommodative with policy and a continuation of solid US earnings results. The previously slumping Real-Estate sector led all S&P sectors for the week, boosted by rising property prices and excellent earnings by one of its largest constituents, Simon Property Group (SPG). The Industrials sector, plagued by rising input costs, lagged all sectors for the week. International equities also finished the week virtually unchanged.

Fixed Income: The yield on the US 10-Year Treasury Note rose above the psychological 3% level during weekly trading for the first time since 2014, before retreating to close out the week up .01% from the prior week at 2.96%. The yield curve flattened out again as short-term rates rose quickly on the release of good economic news, increasing the odds of Federal Reserve tightening. High-yield debt funds recorded outflows as their corresponding spreads over risk-free securities widened slightly. The iShares IBoxx High-Yield Corporate Bond ETF (ticker: HYG) ended the week relatively unchanged to down .1%.

Commodities: Oil prices remain elevated as worries over the Iran deal and the threat of new US sanctions on Iran boil up. All-time highs in US oil production and exports have led to an increasing spread between the International and American oil benchmarks, with International Brent Crude ending up for the week to $74.44 per barrel, while the American West Texas Intermediate price fell slightly to $68.04 per barrel. Natural Gas prices ended the week higher, to $2.77/MMBtu.

WEEKLY ECONOMIC SUMMARY

1st Quarter GDP: The Bureau of Economic Analysis (BEA) released its first estimate for 1st quarter real GDP at an annualized 2.3% quarter-on-quarter (QoQ) growth. This “advance” estimate will be revised two more times as more source data is received, but this initial estimate came in above the consensus at 2.0%. A deceleration in the growth of consumer spending during the quarter is to blame for the slowdown from Q4 2017’s growth of 2.9%, however, 1st quarters have notoriously lagged the other quarters during this recovery. Consumer spending is broadly expected to pick back up in Q2, due to increasing disposable income and high levels of consumer confidence stemming from the tax cuts.

S&P CoreLogic Case-Shiller HPI: The S&P CoreLogic Case-Shiller Home Price Index (HPI) rose another .8% in February on a seasonally adjusted basis. The 2-month lagged index, that tracks changes in value of residential real estate, showed increases in all 20 US metropolitan regions covered. Cleveland and Detroit led all cities with MoM increases of 1.6% and 1.4%, respectively. A tight supply of single-family homes and the strong labor market have contributed to property values continuing to outpace wage growth, as the HPI has increased 6.8% year-on-year (YoY) surpassing the peak of the mid-2000’s to a new record high.

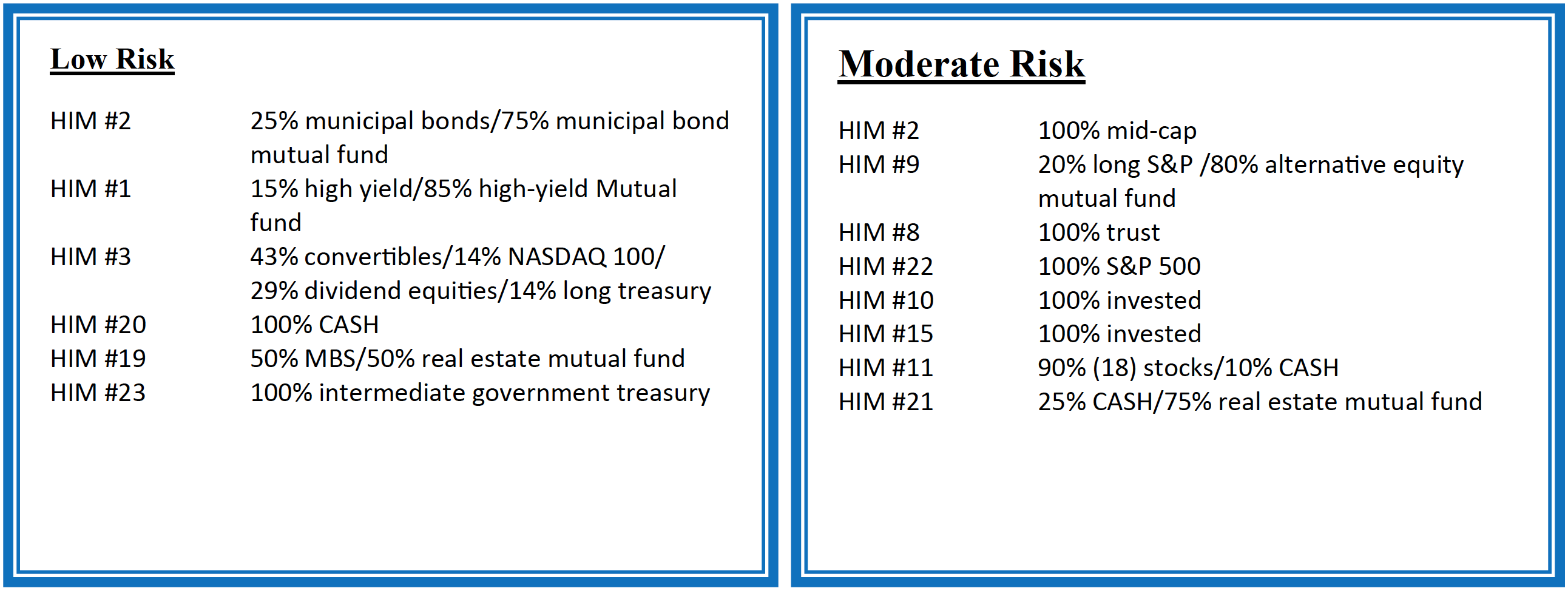

Current Model Allocations

Summary

In utilizing an approach that seeks to limit volatility, it is important to keep perspective of the activity in multiple asset classes. We seek to achieve superior risk-adjusted returns over a full market cycle to a traditional 60% equities / 40% bonds asset allocation. We do this by implementing global mandates of several tactical managers within different risk buckets. For those investors who are unwilling to stomach anything more than minimal downside risk, our goal is to provide a satisfying return over a full market cycle compared to the Barclays Aggregate Bond Index. At Horter Investment Management we realize how confusing the financial markets can be. It is important to keep our clients up to date on what it all means, especially with how it relates to our private wealth managers and their models. We are now in year nine of the most recent bull market, one of

the longest bull markets in U.S. history. At this late stage of the market cycle, it is extremely common for hedged managers to underperform, as they are seeking to limit risk. While none of us know when a market correction will come, even though the movement and volatility sure are starting to act like a correction, our managers have been hired based on our belief that they can accomplish a satisfying return over a full market cycle, – while limiting risk in comparison to a traditional asset allocation approach. At Horter we continue to monitor all of the markets and how our managers are actively managing their portfolios. We remind you there are opportunities to consider with all of our managers. Hopefully this recent market commentary is helpful and thanks for your continued trust and loyalty.