HORTER INVESTMENT MANAGEMENT, LLC

Weekly Commentary horterinvestment.com April 23, 2018

Fed mistakes could spark ‘unusually fast’ bear market, ‘lost decade’ for stocks

Uncertainty over trade policy may be the primary driver of the U.S. stock market at the moment, but the real policy risk facing equities could be coming from the Federal Reserve, with the potential downside a lot more pronounced than investors are currently anticipating.

Last week, Fed Chairman Jerome Powell said the economic outlook had strengthened, but he painted a mixed picture about what policy might look like going forward. The U.S. central bank raised interest rates but indicated it would only do a total of three rate hikes in 2018, which some saw as a dovish signal given that a number of investors had expected four this year. However, the Fed pushed up its expected rate path in 2019 and 2020.

Barry Bannister, head of institutional equity strategy at Stifel, said it was a concern that the Fed’s view for 2019 and 2020 had grown more hawkish, which raised the risk of the central bank making a policy mistake.

“What matters for investors is that any decline is likely to be unusually rapid and occur as a result of P/E compression, resulting from policy risks not weak GDP,” he wrote in a research report. “Investors need a bit more acrophobia, as our best model points to a bear market and lost decade for stocks.”

Bannister argued the new Fed, under Powell, “wishes to fade the ‘Fed put,’” or the idea that the central bank would step in to prop up falling equity prices. “The cost may be a 16% P/E drop,” he wrote, referring to price-to-earnings, a popular measure of equity valuation.

The Fed is expected to regularly raise rates over the coming years, and some investors think it may hasten its pace of increases to rates in the event that inflation returns to the market in a more pronounced fashion.

Investment chief of $250 billion firm says financial markets are on a ‘collision course for disaster’

Investors should brace themselves for a vicious recession made worse by large corporate debt levels, according to Guggenheim’s Scott Minerd.

He warned clients that inflation and rate hikes from the Federal Reservewill lead to the next market downturn.

“I have come to realize that the markets are potentially on a collision course for disaster. The collision course is being brought about by strong fiscal stimulus in the late stage of the business cycle, when conventional economic wisdom mandates that it should be heading the other direction to create fiscal drag,” the firm’s global chief investment officer wrote in a note to clients Monday. “With the huge fiscal stimulus coming online, the Federal Open Market Committee (FOMC) will feel obliged to play the role of creating economic headwinds.”

Guggenheim has more than $250 billion in assets under management across its fixed income, equity and alternative investment strategies, according to its website.

Taking a comprehensive look at the overall current stock market

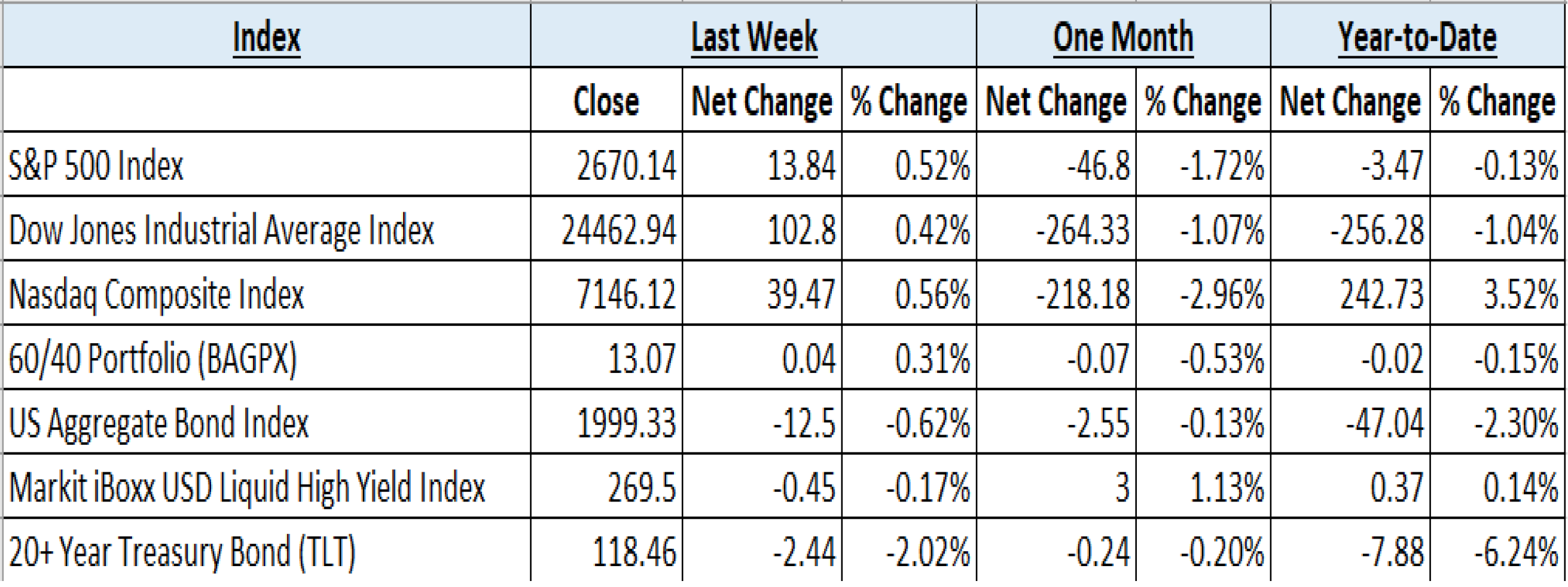

Taking a comprehensive look at the overall current stock market, you can see the chart below representing eight major indices and their returns through the week ending April 20, 2018. In a truly diversified portfolio, the portfolio’s total return is determined by the performance of all of the individual positions in combination – not individually.

So, understanding the combined overall performance of the indices below, simply average the 7 indices to get a better overall picture of the market. The combined average of all 7 indices is –0.89% year to date.

Data Source: Investors FastTrack, Yahoo Finance

Past performance is not a guarantee of future results. This Update is limited to the dissemination of general information pertaining to its investment advisory services and is not suitable for everyone. The information contained herein should not be construed as personalized investment advice. There is no guarantee that the views and opinions expressed in this newsletter will come to pass. Investing in the stock and bond markets involves gains and losses and may not be suitable for all investors. Information presented herein is subject to change without notice. Horter has experienced periods of underperformance in the past and may also in the future. The returns represented herein are total return inclusive of reinvesting all interest and dividends.

The above equity, bond and cash weightings are targets and may not be the exact current weightings in any particular client account. Specifically, there may be cases where accounts hold higher cash levels than stated in these target weightings. This is usually to accommodate account level activity. Furthermore, some variable annuity and variable universal life accounts may not be able to purchase the exact weightings that we are indicating above due to specific product restrictions, limitations, riders, etc. Please refer to your client accounts for more specifics or call your Horter Investment Management, LLC at (513) 984-9933.

Investment advisory services offered through Horter Investment Management, LLC, a SEC-Registered Investment Advisor. Horter Investment Management does not provide legal or tax advice. Investment Advisor Representatives of Horter Investment Management may only conduct business with residents of the states and jurisdictions in which they are properly registered or exempt from registration requirements. Insurance and annuity products are sold separately through Horter Financial Strategies, LLC. Securities transactions for Horter Investment Management clients are placed through TCA by E*TRADE, TD Ameritrade and Nationwide Advisory Solutions.

For additional information about Horter Investment Management, LLC, including fees and services, send for our disclosure statement as set forth on Form ADV from Horter Investment Management, LLC using the contact information herein. Please read the disclosure statement carefully before you invest or send money.

Dow Jones – Week Ending

WEEKLY MARKET SUMMARY

Global Equities: US Equities ended the week with modest gains, helped by a strong start to the 1st quarter earnings season that had already high expectations. The Nasdaq Composite Index gained about .6%, followed by the S&P 500 up near .5%, and the Dow Jones Industrial near .4%. The Energy sector has stayed hot by leading all S&P sectors for the week, while Consumer Staples lagged all sectors. International equities underperformed their US counterparts, with Emerging Markets and Developed-market International equities both down marginally for the week.

Fixed Income: The yield on the US 10-Year Treasury Note increased steadily, matching the February high of 2.95%, as a slew of Federal Reserve members gave speeches throughout the week. After consistent flattening, the Treasury yield curve is finally starting to show some life as the spread between 10-Year and the 2-Year widened to .53% from .47% at the beginning of the week. High-yield debt funds recorded this year’s largest inflows as their corresponding spreads over risk-free securities tightened to January lows mid-week, before widening to the prior week levels. The iShares IBoxx High-Yield Corporate Bond ETF (ticker: HYG) ended the week down around .4%.

Commodities: Geopolitical concerns have helped oil prices reach multi-year highs. A tweet from President Trump directly attacking OPEC for manipulating prices was brushed aside as Brent Crude closed the week up around 2% to nearly $74 per barrel. American oil companies must surely be enjoying the rally, as the US benchmark West Texas Intermediate increased nearly 1.5% during the week to $68.38 per barrel, despite an increasing rig count. Natural Gas prices ended the week virtually unchanged near $2.74/MMBtu.

WEEKLY ECONOMIC SUMMARY

Leading Economic Index (LEI): The Conference Board released LEI rose .3% for the month of March. While smaller than it has been in recent months, the increase signals continued solid US growth for the rest of the year. Negative contributors from a softening in employment data were more than cancelled out by positive readings for the interest rate spread, ISM new orders, average consumer expectations for business conditions, building permits, the Leading Credit Index, and manufacturers’ new orders for consumer goods and materials. The Conference Board Coincident and Lagging Economic Indexes for the US also increased during the period at rates of .2% and .1%, respectively.

Fed Beige Book: The tone of the Beige Book echoes the previous release with a continued modest to moderate outlook on increasing economic activity and price pressure across the 12 districts covered. Tight labor-market conditions continue as shortages were again being reported for high-skill positions in engineering, information technology, healthcare, and construction. There was a noteworthy addition to the report, however, with wide-spread indications of rising steel prices, sometimes “dramatically” so, due to the new tariffs. Overall, this is another Beige Book that is not indicative of increasing the pace of rate hikes when the Federal Reserve board meets under a fortnight.

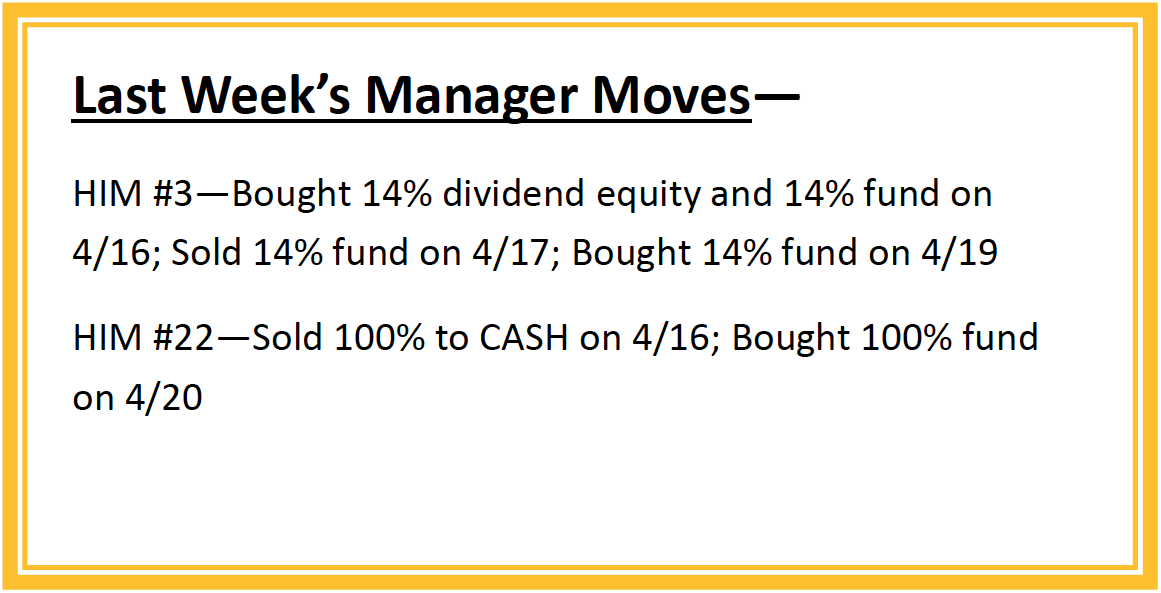

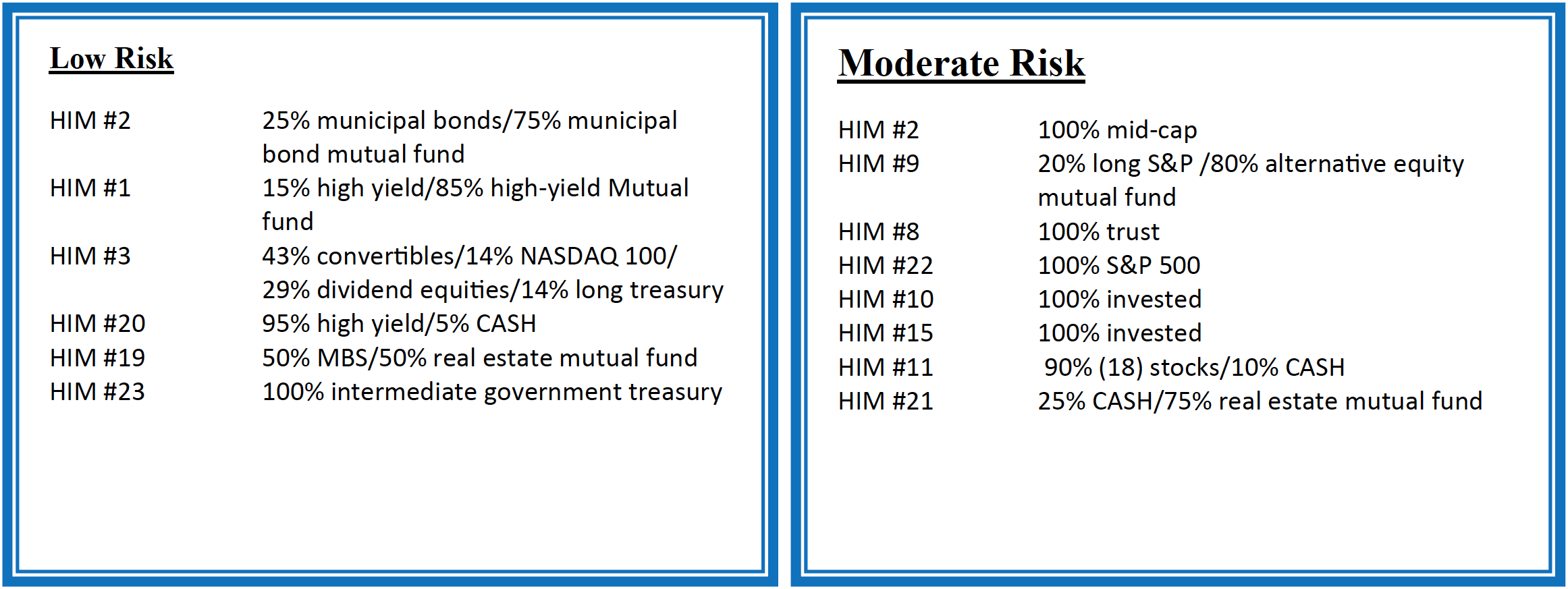

Current Model Allocations

Summary

In utilizing an approach that seeks to limit volatility, it is important to keep perspective of the activity in multiple asset classes. We seek to achieve superior risk-adjusted returns over a full market cycle to a traditional 60% equities / 40% bonds asset allocation. We do this by implementing global mandates of several tactical managers within different risk buckets. For those investors who are unwilling to stomach anything more than minimal downside risk, our goal is to provide a satisfying return over a full market cycle compared to the Barclays Aggregate Bond Index. At Horter Investment Management we realize how confusing the financial markets can be. It is important to keep our clients up to date on what it all means, especially with how it relates to our private wealth managers and their models. We are now in year nine of the most recent bull market, one of

the longest bull markets in U.S. history. At this late stage of the market cycle, it is extremely common for hedged managers to underperform, as they are seeking to limit risk. While none of us know when a market correction will come, even though the movement and volatility sure are starting to act like a correction, our managers have been hired based on our belief that they can accomplish a satisfying return over a full market cycle, – while limiting risk in comparison to a traditional asset allocation approach. At Horter we continue to monitor all of the markets and how our managers are actively managing their portfolios. We remind you there are opportunities to consider with all of our managers. Hopefully this recent market commentary is helpful and thanks for your continued trust and loyalty.