One of the Most Remarkable Market Trips in History

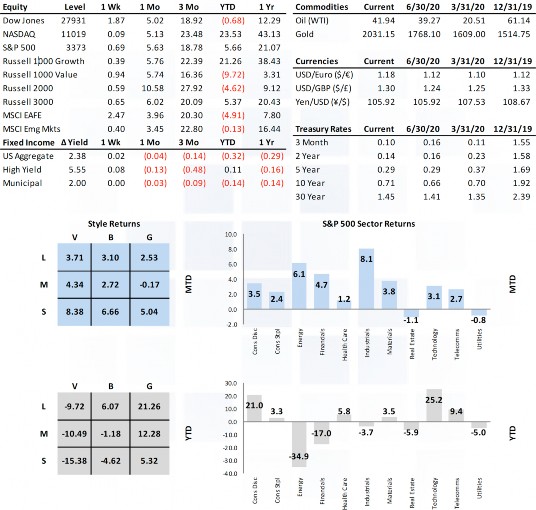

Global equity indices marked new record highs last week, capping off what has truly been one of the most remarkable market round trips in history. The Bloomberg World Equity Index fell over 30% in a month last spring and went on to rally 45% over the following five months. The S&P 500 came within a whisper of its February high on an intraday basis with smaller caps and cyclicals (industrials, energy, materials) leading the way as participation continued to broaden out. Treasuries had a rough week with long yields climbing nearly 20bps in a steepening yield curve. Gold snapped a nine-week win streak, falling 4.3%.

Market Anecdotes

• Bespoke noted last week marked 100 days since the March lows during which the S&P 500 rallied 51.3%, a 100-day rally magnitude that we’ve not seen since 1933.

• While U.S. markets are back at record high levels, Europe’s STOXX 600 is still down more than 10% from its 2020 high (local FX terms) and the Nikkei is 5% below its January high.

• It sounds bizarre but technology is the sixth best performing sector here in 3Q with industrials (transports), materials, and consumer discretionary leading the way. Act IV?

• 2Q earnings season is largely behind us with over 90% of companies reporting. With an e-beat rate over 80% we can firmly categorize the quarter as far better than expected.

• Real estate casualties of COVID are beginning to emerge. Manhattan apartment vacancies hit a record 4.33% in July, new leases in NW Queens fell 60% with median rent rates falling 15%. Macys is expected to vacate its Mag Mile location in Chicago.

• CRE loans are much more pronounced in smaller regional and community banks (28%) than they are for larger banks (13%) according to the FDIC.

• The leveraged loan index has recovered from the high 70’s to the low 90s since March but default rates have climbed from 0.87% to 3.70% while high yield bond defaults have climbed above 6%.

• POTUS executive orders last week assured markets and should garner goodwill at the polls, but legality, practicality and efficacy are in question. There is only $44 billion of available federal money for unemployment benefits and states wherewithal to fund the rest makes clear the need for congress and the senate to act to avoid fiscal tightening.

• Strategas notes global central bank balance sheets are growing 33% YoY, driven mostly by the ECB and BoJ (Fed has stalled at around $7b since middle May). Additionally, money supply (M2 YoY) is growing at a 23% clip.

• COVID trends in the U.S. continue to drift lower including a 7.31% positivity rate (lowest since July 1st), average daily rate of new cases (lowest levels since 7/7), while deaths and hospitalizations decline as well. Meanwhile, other countries have started to see renewed upticks including India, Japan, Germany, France, and Spain.

Economic Release Highlights

• U.S. retails sales growth of 1.2% missed expectations for 2.1% growth but put spending back to pre-COVID levels and actually beat on ex-Autos (1.9% v 1.3%) and ex-Autos & Gas (1.5% v 1.0%). June was also revised notably higher as well from 7.5% to 8.4%.

• The JOLTS (Job Opening and Labor Turnover Survey) showed an increase in U.S. job openings in June, rising to 5.9mm, only 5.288mm was expected. Initial jobless claims of 963k is the first time we’ve been below 1mm since March.

• NFIB Small Business Optimism registered 98.8, shy of expectations of 100 and last month’s 100.6 reading.

• UofM consumer sentiment changed little, moving from 72.5 to 72.8 in early August.

• CPI headline and core came in slightly higher than expectations with readings of 1.0% and 1.6% respectively.

• PPI came in higher than expected (0.6%a vs 0.3%e) but was shrugged off and didn’t have any impact on futures markets.

W E E K E N D I N G 8 / 14 / 2 0

INSIGHT

MARKET ANALYSIS