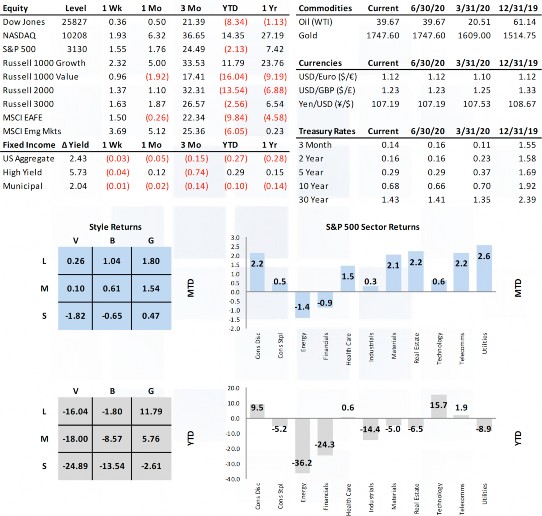

NASDAQ Finishes at New Record as Markets Rally.

Markets shrugged off the prior week of rising coronavirus anxiety, instead choosing to embrace encouraging economic reports during last week’s holiday shortened 4-day trading session. The NASDAQ posted its biggest weekly gain since early May, finishing at a new all-time high while the S&P 500 tacked on over 4% with all sectors finishing in the black. Commodity markets benefited from a 5% rally in oil prices which closed over $40, longer term interest rates moved slightly higher, and the USD weakened marginally primarily against commodity currencies.

Market Anecdotes

• Bespoke noted the 33% decline in 33 calendar days leading to March 23rd was followed by a 40% rally in 100 calendar days that followed, the strongest 100-day return since 1933.

• FOMC meeting minutes and the speaking circuit shone a light on conversations surrounding yield curve control and stronger forward guidance on the part of the Fed.

• The impact of recent Fed activity in the financial markets made several headlines last week as they became a top 5 holder of some of the most prevalent publicly traded fixed income ETFs.

• Bespoke made note of the cycle of U.S. to international equity markets, highlighting longer term trends, technical support levels, and fundamental cases for some mean reversion.

• Acceleration of real M1 growth in Europe is consistent with a sharp pickup in economic activity in late 2020 and early 2021. This, combined with better CoVid-19 wave risk management, improves the outlook for European GDP relative to the U.S.

• Pfizer gave markets a boost of Covid19 confidence on positive news surrounding their leading vaccine trials. Globally 17 vaccines are in human trial stages with 130 others in development.

• Don Rissmiller from Strategas suggested Covid-19 recession #1 (March-May) is over, while the lingering effects of high unemployment and economic costs of rolling coronavirus waves pose challenges to the second phase of the business cycle recovery.

• Historically economic shocks lead to surges in nationalism and policy uncertainty. After an unprecedented surge in globalization, conditions in China, India, and Russia may determine the global course more so than the U.S.

• The D’s renewed stimulus proposal is worth $3 trillion, plus an infrastructure bill that nominally amounts to $500 billion over five years.

• BCA projects the U.S. consumer fiscal “cliff” created by the one-time stimulus checks will require close to $1t boost to personal income to prevent falling below February levels.

• The PPP deadline was extended last week to allow more time for businesses to complete registration while the MSLP, launched 6/15, has seen only sparse interest on behalf of lenders.

• U.S. WTI inventories fell 7.2mb last week, far more than the 100,000 forecasted, supporting oil prices in spite of KSI threats of commencing a price war with non-compliant members. Economic Release Highlights

• Consumer confidence jumped from 85.9 to 98.1, far surpassing consensus calls for 90 and improved in both present situation and expectations sub-components.

• April’s Case-Shiller HPI rose 0.3% MoM and 4% YoY, both relatively in line with expectations.

• June’s U.S. PMI manufacturing index jumped to 49.8 from 39.8 the prior month.

• June’s U.S. ISM manufacturing index jumped into expansionary territory of 52.6 from 43.1 the prior month.

• June payrolls of 4.8mm (3.0mm forecasted) followed up May’s shocking upside surprise report of 2.5mm. The unemployment rate dropped to 11.1% from 13.3%.

• Pending home sales in May increased 44.3%, far in excess of the 11.3% expectation.

• AAII weekly sentiment survey registered just a 22.15% bullish reading, a fourth consecutive weekly decline leaving it at its lowest level since October 2019.

INSIGHT

MARKET ANALYSIS