Equity Markets Post Healthy Gains Closing Strong

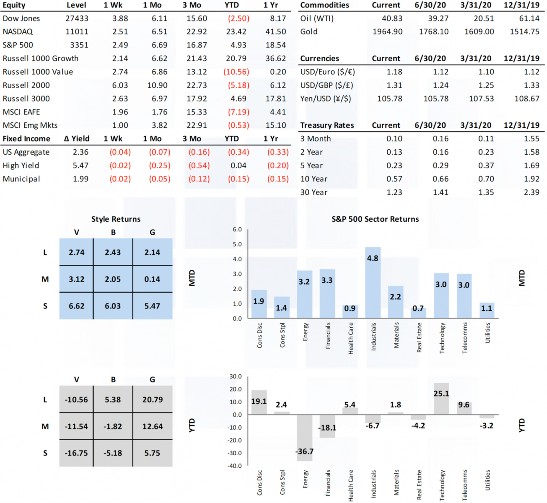

Last week, equity markets bolted on to some already pretty gaudy results of the past several weeks, coming within 1% of February’s record high on an intraday basis. The first full week of August felt pretty bullish with all U.S. equity classes and sectors posting healthy gains and only Brazil was left out of the non-U.S. equity market rally. Market internals last week favored cyclicals (industrials, financials, energy) over defensives (health care, utilities, consumer staples).

Market Anecdotes

• DC negotiators failed to reach a stimulus deal and remained pretty far apart (trillions of dollars and different sets of facts). POTUS executive orders were expected to bridge the gap over the weekend which is why markets are remaining calm for now.

• COVID data seems to be taking a modestly positive turn over the past two weeks. Confirmed cases have fallen 18% since July 23 while positivity rates, deaths, and hospitalization rates are falling as well.

• Despite a significant mega cap tech rally late last week, this week saw value and smaller caps lead the way.

• Earnings season is maintaining a clear positive skew with earnings and sales beat rates of 68% and 62%. A net guidance spread of +18.6% is also extraordinarily positive.

• Ned Davis pointed out, on average, the stock market bottoms four months prior to the end of recession and earnings/revenue bottom six and nine months after the end of recession.

• Bloomberg highlighted at least 25 major retailers have gone BK this year. Chapter 11 allows them to walk away from leases translating to CMBS delinquencies, now 16% from 3.8% in Jan.

• A 2Q NY Fed report shows total household debt declining for the first time since 2014. Credit card balances fell $76b, the steepest margin on record while mortgage balances fell by $63b.

• The big story on Tuesday was the 2% rally in gold that pushed the December futures contract to a new record high of $2,027.30. Negative real rates, particularly with the U.S. joining that club have factored materially into the picture for gold.

• The USD is down 10% from its March highs, now below 93 for the first time since May 2018.

• The BCA Pipeline Inflation Indicator has troughed suggesting bond yields have limited downside risk looking forward.

Economic Release Highlights

• The July jobs report was solid at 1.76mm (1.675mm expected) and the unemployment rate falling to 10.2%. U-6 under-employment rate fell to 16.5% and participation stalled out at 61.4%.

• All but three of eleven major global services and manufacturing PMIs moved back into expansionary territory.

• July PMI (50.9a vs 51.3e) and ISM (58.1a vs 55e) manufacturing indices both marked improvement over the prior months, now both officially residing in expansionary territory.

• July PMI (50.0a vs 49.6e) and ISM (54.2a vs 53.5e) services indices both marked improvement over the prior months, now both officially residing in expansionary territory.

• The ISM commodities survey pointed to upside price risk across the commodity markets with a +20 net reading, the highest since October 2018 and the fourth highest ‘short supply’ response (24) on record.

• Initial jobless claims (weekly) declined to 1.186mm from last week’s 1.435mm but still sit two-times higher than what we saw during the GFC.

• July motor vehicle sales of 14.5mm (11.2 domestic) grew handily over June’s 13.1mm and came in well over expectations of 14.0mm.

W E E K E N D I N G 8 / 07 / 2 0

INSIGHT

MARKET ANALYSIS