US Markets Close Out July on Strong Note

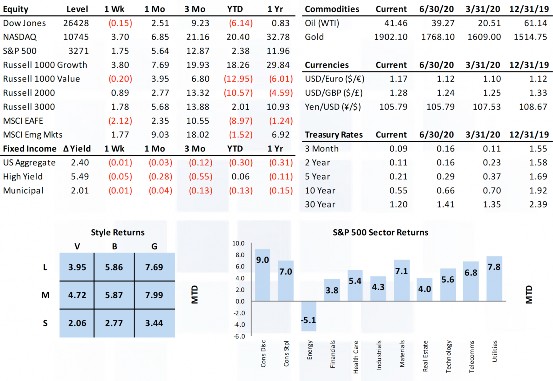

Equity markets closed out July on a strong note with the S&P 500 up 1.7% while international and emerging markets were down. European stocks fell 3% on the week. Mega cap growth stocks plowed through Congressional interrogations and posted strong earnings to lead markets higher but cyclical areas of the market (energy, materials, financials) lagged. A federal fiscal stimulus renewal package remained elusive to and through expiration of enhanced benefits on Friday. Commodities lost 0.64% driven by oil moving back toward the $40 range but gold continued its march higher, +3.3% last week. Rates moved lower in a parallel fashion leaving the 10yr UST at 0.55% and the USD fell 1.15%.

Market Anecdotes

• The stock market shrugged off fiscal inaction in DC, sustained CoVid-19 wave data, and a grilling of tech execs in DC, giving way to encouraging earnings and economic reports.

• Virus news seems to be slowly transitioning to a less threatening trajectory with new case averages and CoVid-19 doctor visits finally turning back down.

• Over 700 companies had reported through Thursday. FactSet is reporting earnings beat rate of 84% on a -35.7% bottom line.

• Fiscal stimulus negotiations missed the 7/31 soft deadline, as Congress adjourned last Thursday. Recess ends 8/3 and the hope is they make quick work of meeting in the middle.

• While the negative incentive of increased unemployment benefits is clear, that assumes employers are hiring with ample job openings but job openings are currently 23% lower than the beginning of the year, making a strong case for demand stimulus checks of any sort.

• Does the parabolic increase in government debt portend disaster with gold rallying and the USD falling? Not yet says BCA. If disaster was imminent, it is highly unlikely we would have a 0.55% 10yr and 1.20% 30yr UST yields. Inflation recalibrating? Probably.

• Last week saw gold eclipse the prior record high of $1920.7 back in September 2011.

• The Fed meeting last week produced no surprises. QE forever, a twinkie will decompose before they raise rates, and they see no negative implications of these policies whatsoever.

• The Fed balance sheet has stalled at around $7tn, actually declining $15.7b since May 13th.

• More positive homebuilders news with DHI beating by 31% on the bottom line and 3.6% on the top with encouraging closings, orders, and backlog data as well.

• The tech sector weighting is now over 27%, just shy of the ‘99 29.18% high water mark. Energy slipped to 2.5%, a new record low and far below the 13.14% weight in 2008.

• ICI released MF/ETF flows through June, confirming bond product took in flows of over $100b, a record amount.

• AAII bullish sentiment fell to 20.23%, a lower level than at any time during the CoVid-19 crisis. Bearish sentiment sits at 48.47%, just 3.6% below the 3/26 reading which climbed over 50%.

Economic Release Highlights

• Q2 U.S. GDP dropped a record 9.5% QoQ and 32.9% YoY in what the IMF has coined “The Great Lockdown”.

• June personal income fell 1.1% in June (after -4.4% in May) but consumer spending increased +5.6% on the month.

• Initial jobless claims moved higher last week to 1.4mm in the July 25th week and continuing claims rose to 17.0mm (for the week prior).

• Durable goods orders rose 7.3% in June (only 5.4% expected), driven by a surge in vehicle orders. Ex-transports and ex-aircraft both rose a more modest 3.3%.

• Real-time activity data such as mobility data, restaurant reservations, airport travel stats, and the NY Fed weekly index have faded in July alongside the CoVid-19 resurgence.

• UofM consumer confidence softened in July to 72.5.

W E E K E N D I N G 7 / 31 / 2 0

INSIGHT

MARKET ANALYSIS